The FIRE Number: How Much Money Do You Actually Need to Retire Early?

⚡ Key Takeaways: Your FIRE Number

- Your FIRE number is the total investment portfolio you need to retire early and never run out of money — typically 25x your annual expenses.

- The 4% rule is the foundation: withdraw 4% of your portfolio per year and it will likely last 30+ years.

- Reducing expenses has a double effect — it lowers your FIRE number AND frees up more money to invest.

- A $60,000/year lifestyle requires a $1.5M portfolio. A $40,000/year lifestyle requires only $1M.

- Your FIRE number is personal — healthcare costs, location, risk tolerance, and timeline all affect it.

By Jamie Park | Aedilis

I used to think retirement was something that happened at 65 — automatically, like a switch flipping. You work, you get old, you stop working. The end.

Then I learned about the FIRE number, and my whole mental model broke open.

FIRE stands for Financial Independence, Retire Early. The premise is simple: if your investments generate more money than you spend, you never need to work again. You’re financially free. And the number that makes that happen? That’s your FIRE number.

The 4% Rule: Where the Math Comes From

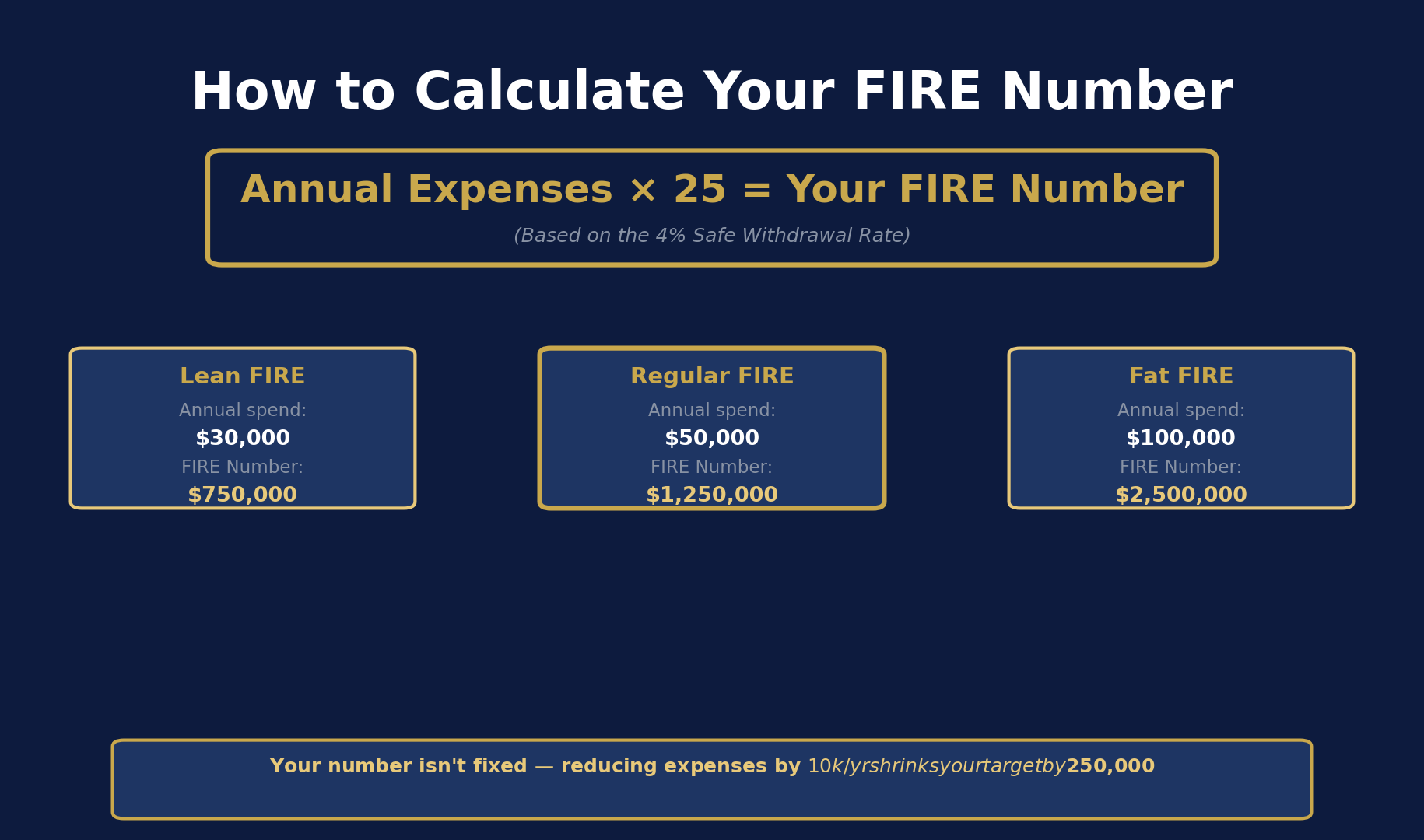

Your FIRE number = your annual expenses × 25.

This comes from the Trinity Study, a landmark 1998 analysis of historical stock market returns showing that a portfolio of 50-75% stocks can sustain a 4% annual withdrawal rate for 30+ years without running out of money — through recessions, crashes, and inflation — about 95% of the time.

In other words: if you have 25× your annual expenses invested, you can withdraw 4% per year and statistically expect to never run out of money.

Your Number in Practice

- Spend $30,000/year → FIRE number: $750,000

- Spend $50,000/year → FIRE number: $1,250,000

- Spend $75,000/year → FIRE number: $1,875,000

- Spend $100,000/year → FIRE number: $2,500,000

Notice that lowering your expenses does two things at once: it reduces your FIRE number (smaller target) AND increases how much you can save each year (faster progress). This is why frugality has compounding benefits in the FIRE math.

Three Versions of FIRE

Lean FIRE — Living on $25,000-$40,000/year. Requires a FIRE number of $625k-$1M. Achievable faster, but leaves little room for lifestyle inflation.

Regular FIRE — $50,000-$75,000/year. FIRE number of $1.25M-$1.875M. Most common target for people with average-to-comfortable lifestyles.

Fat FIRE — $100,000+/year. FIRE number of $2.5M+. Full financial freedom with no lifestyle compromise.

Not sure which tier fits your life? Compare Lean vs. Fat vs. Barista FIRE side by side.

There’s also Coast FIRE — where you front-load saving early and let compound growth carry you to your number without adding another dollar.

The Savings Rate Is the Variable That Matters Most

Here’s what blew my mind: how fast you reach your FIRE number depends almost entirely on your savings rate, not your income. Someone saving 50% of a $60,000 income will reach FIRE faster than someone saving 10% of a $200,000 income.

- Save 10% → ~46 years to FIRE

- Save 25% → ~32 years

- Save 50% → ~17 years

- Save 70% → ~8.5 years

The math doesn’t lie. Every extra percentage point of savings rate cuts years off the timeline.

The Next Step

Calculate your annual spending. Multiply by 25. That’s your FIRE number. Then figure out your current savings rate. That tells you when you’ll get there — and whether you want to change the timeline. For age-specific targets, see these net worth benchmarks for W2 employees. For a broader, non-W2 view, see the honest net worth benchmarks by age.

You don’t have to want Lean FIRE or Fat FIRE. You just need to know your number. Once you do, financial independence stops being a dream and starts being a math problem — and math problems have answers.

Frequently Asked Questions: Your FIRE Number

What is a FIRE number?

Your FIRE number is the total portfolio value you need to retire early and live off investment returns indefinitely. It’s calculated by multiplying your expected annual spending by 25 — based on the 4% safe withdrawal rate. If you plan to spend $50,000/year in retirement, your FIRE number is $1.25 million.

What is the 4% rule and is it still valid?

The 4% rule comes from the Trinity Study, which analyzed historical market data and found that withdrawing 4% of your portfolio annually — adjusted for inflation — had a very high success rate over 30-year periods. Many FIRE researchers now suggest 3.5% for longer retirements (40+ years). It’s a guideline, not a guarantee, but it’s the most widely tested rule for retirement portfolio sustainability.

Does my FIRE number include Social Security?

It doesn’t have to. Many early retirees calculate their FIRE number without Social Security because they plan to retire decades before they can collect it. If you retire at 40 and Social Security kicks in at 67, you’re covering a 27-year gap yourself. Once Social Security starts, your withdrawal rate from your portfolio can drop, making your money last longer than the 4% rule alone suggests.

Curious what an aggressive early target looks like in practice? Here is the real math behind retiring at 45.

What if my expenses change after I retire?

They will — plan for it. Healthcare is the biggest wildcard for early retirees since you’re off employer coverage. Most FIRE planners model a “go-go” phase of higher spending early in retirement, a “slow-go” middle phase, and a “no-go” phase of lower spending later. Adding a 10-15% buffer to your FIRE number accounts for this variability without dramatically delaying your target date. 2026 update: The enhanced ACA marketplace subsidies that kept premiums low for early retirees expired December 31, 2025 — budget for potentially $16,000+/year more in healthcare costs if you plan to bridge to Medicare on marketplace coverage.

How do I calculate my personal FIRE number?

Track your spending for 3 months and annualize it. That’s your baseline annual expense figure. Adjust for any expected retirement lifestyle changes (no commute costs, but more travel). Multiply that number by 25 for a standard 4% withdrawal rate, or by 28-30 if you want more safety margin. That’s your FIRE number. It will change as your spending and life circumstances evolve — recalculate it annually.