The Aedilis Stack: The 6 Financial Moves Every W2 Employee Should Make

⚡ Key Takeaways: The Aedilis Stack

- There is a specific sequence to financial moves that matters — doing them out of order costs you money and time.

- Maxing your 401(k) cuts your taxable income immediately — a $24,500 contribution saves ~$5,170 in taxes at the 22% bracket.

- The HSA is the only account in the tax code that gives you three separate tax breaks at once.

- A Backdoor Roth IRA lets high earners access Roth benefits even above the income limit.

- Side income accelerates every layer of the stack — even $500/month invested changes your FIRE timeline by years.

By Maya Chen | Aedilis

I was 32 years old, making decent money as a registered nurse, and I was doing everything wrong. I had $45,000 in student loans, no idea where my paycheck was going, and I’d never bought a single stock in my life.

Then I realized something that changed everything: wealthy people aren’t smarter than me. They just know the sequence.

Six years later, I had my loans paid off, an $800,000 portfolio, a rental property that cash flows $800 every month, and I was financially independent at 38.

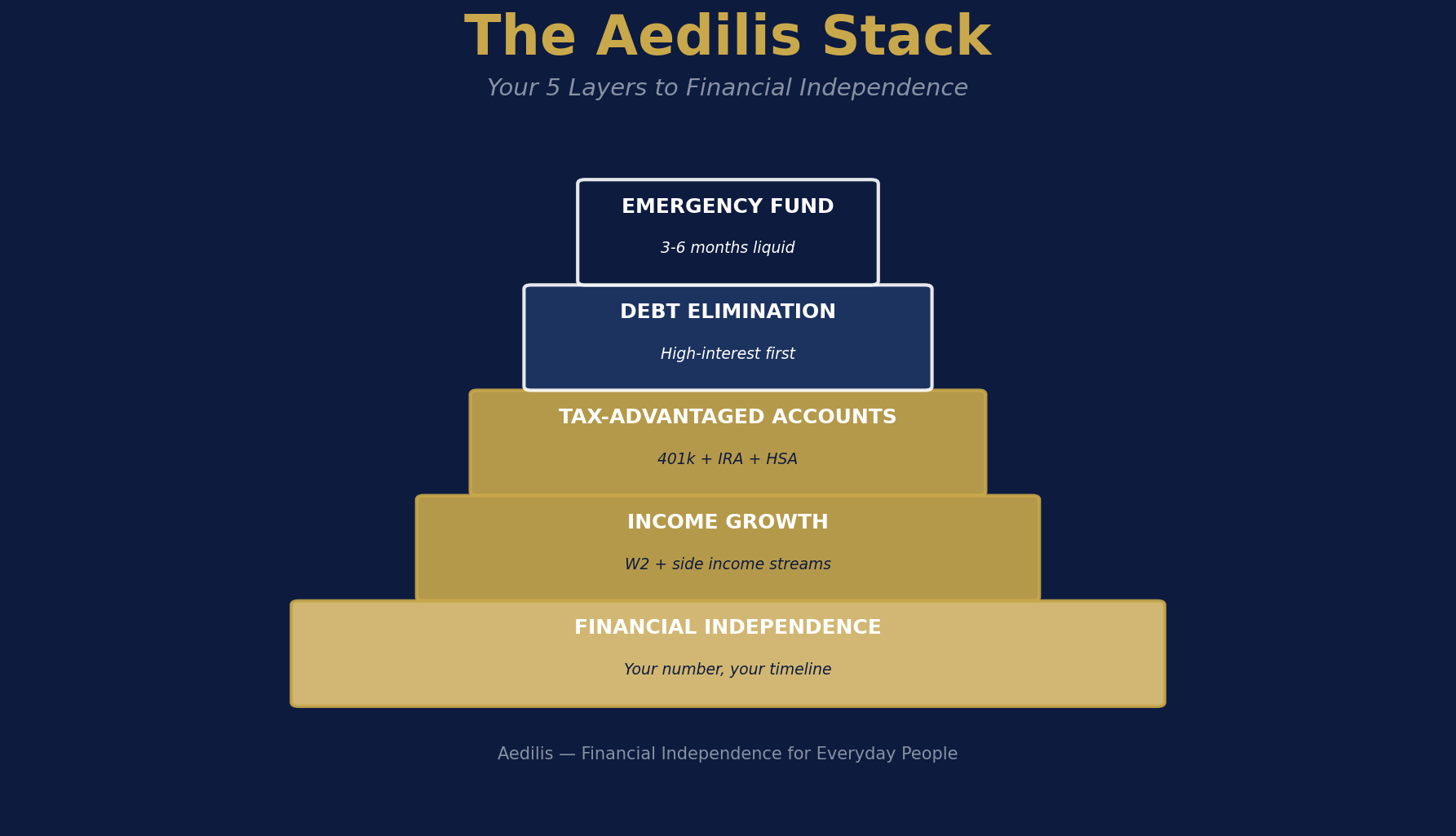

Layer 1: Maximize Your 401k and Get the Match

If you make $80,000 and contribute $23,000 to your 401k, you only pay taxes on $57,000. That’s a $5,060 tax break at the 22% bracket — immediately, that year. Plus your employer match is free money.

Layer 2: Build an Emergency Fund and Eliminate High-Interest Debt

Four months of expenses in a high-yield savings account before investing a single extra dollar. High-interest debt — credit cards, personal loans — cancels out any investment gains you make.

Layer 3: Max Out Tax-Advantaged Accounts (HSA, Roth IRA)

The HSA is the only triple-tax-advantaged account that exists: pre-tax contributions, tax-free growth, tax-free withdrawals for medical expenses. The Roth IRA locks in your current tax rate on contributions, then grows tax-free forever.

Layer 4: Invest in Index Funds and Buy Real Estate

You’re not gambling — you’re buying a tiny piece of thousands of companies. Consistent monthly investment beats timing the market every time. My duplex cash flows $800/month while tenants pay down my mortgage.

Layer 5: Side Income and Advanced Tax Strategy

A side business opens up deductions: home office, equipment, a portion of utilities. (Even without one, most W2 employees miss several deductions they already qualify for.) Once you have multiple income streams, an accountant pays for itself many times over.

Layer 6: Advanced Structures and Estate Planning

Once you’ve built $1M+ in assets, trusts and entity structures become worth exploring. But you don’t start there. You start with Layer 1.

The sequence works. Pick Layer 1. Do it this month. Six years from now, you’ll be amazed at where you are.

Frequently Asked Questions: The Aedilis Stack

What is the Aedilis Stack?

The Aedilis Stack is a layered framework for building wealth as a W2 employee — in the right order. It prioritizes tax-advantaged accounts first (401k, HSA, Roth IRA), then taxable investing, then side income and real estate. Doing the layers in sequence means each move builds on the last and you never waste money doing step 5 before step 2.

Should I invest before paying off debt?

It depends on the interest rate. High-interest debt (above 7%) should be paid off first — the guaranteed return of eliminating that debt beats most market returns. Low-interest debt (below 4%) is fine to carry while investing, since your investment returns will likely exceed the interest cost. Everything in between is a judgment call based on your risk tolerance.

What if I can’t max out my 401(k) right now?

Start with enough to capture your full employer match — that’s a guaranteed 50-100% return depending on your company’s matching formula. Then increase your contribution by 1% every time you get a raise. Most people don’t notice the difference in their paycheck, and over years it compounds to a full contribution.

What’s the difference between a Roth IRA and a Traditional IRA for a W2 employee?

A Traditional IRA may give you a tax deduction now (depending on your income and whether you have a 401k), and you pay taxes when you withdraw in retirement. A Roth IRA gives you no deduction now, but withdrawals in retirement are completely tax-free. For most early-career W2 employees in lower brackets, the Roth wins. For high earners, the Backdoor Roth is the workaround.

How long does it take to become financially independent on a W2 salary?

That depends on your savings rate. At a 10% savings rate, it takes roughly 40+ years. At 30%, about 25 years. At 50%, closer to 15 years. Track your progress against age-based net worth benchmarks to see if you’re on pace. Compare yourself to the honest net worth benchmarks by age too. The Aedilis Stack is designed to systematically increase your savings rate over time — each layer frees up more money and reduces your tax burden, making the next layer easier to fund.