Index Funds for Beginners: The Honest Guide I Wish I’d Had

By Jamie Park | Aedilis

I avoided investing for three years because I was scared of the stock market. I thought it was gambling. I thought you had to be smart about finance to do it. I thought I’d lose everything.

None of that was true. Here’s what I wish someone had told me.

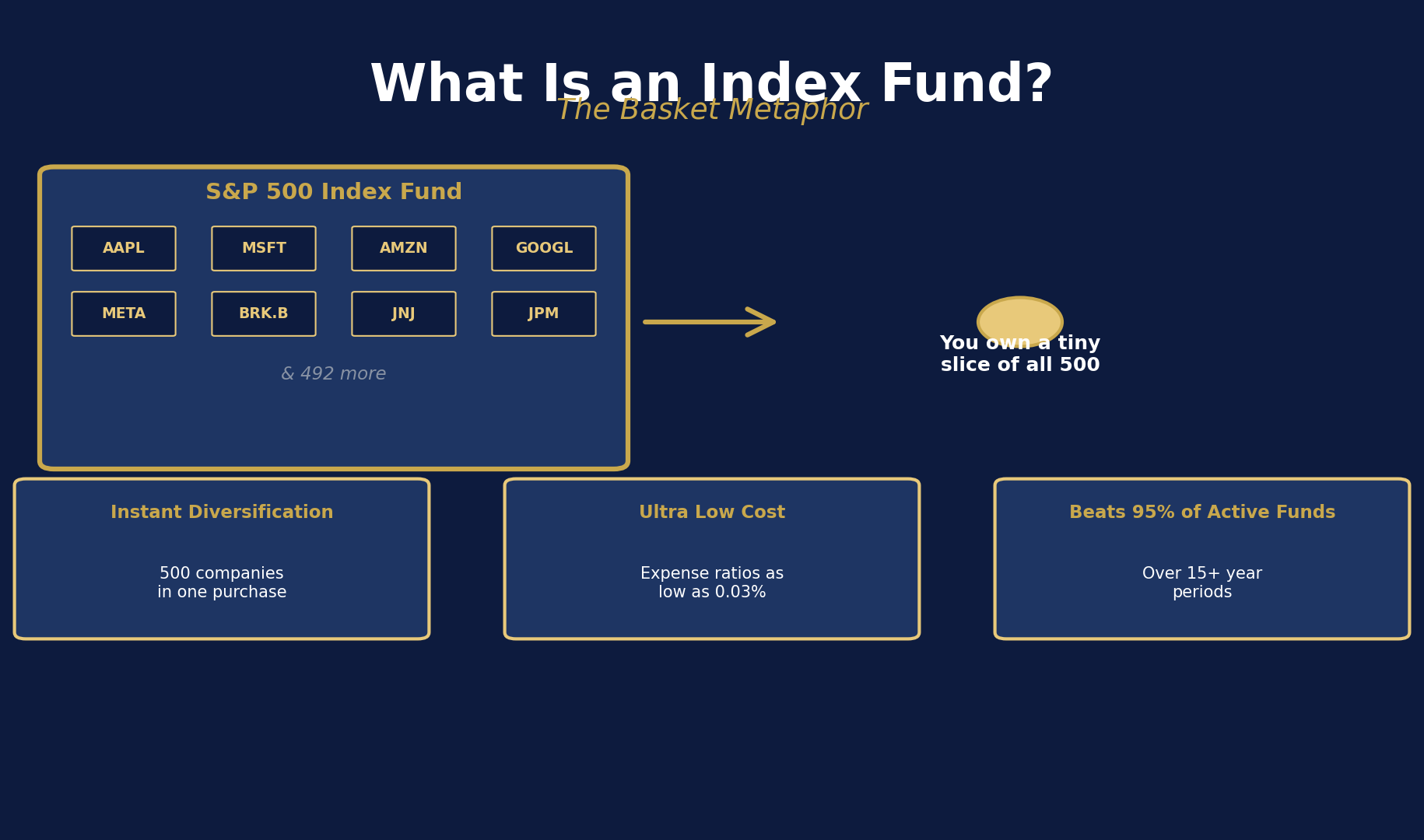

What an Index Fund Actually Is

An index fund is a single investment that automatically owns a small piece of hundreds or thousands of companies. When you buy one share of a total U.S. market index fund, you own a tiny slice of Apple, Microsoft, Amazon, and 3,500+ other companies.

You’re not betting on one company. You’re betting on all of them — on the broad health of the economy. If one company goes bankrupt, it barely moves the needle. For the whole fund to fail, the entire economy would have to collapse permanently.

Why Index Funds Beat Active Management

About 90% of actively managed funds underperform their benchmark index over 15-year periods. Meaning: a professional whose entire job is picking stocks fails to beat the simple “buy everything” approach most of the time.

Why? Fees. An actively managed fund might charge 0.75%-1.5% per year. A [Vanguard](https://investor.vanguard.com/?ref=aedilis) or [Fidelity](https://www.fidelity.com/?ref=aedilis) index fund charges 0.03%-0.10%. Over 30 years, that 1% difference on a $500,000 portfolio costs you over $180,000 in lost returns.

The Three Index Funds That Cover Everything

- Total U.S. Market (VTI or FSKAX) — Every publicly traded U.S. company. The bedrock of most portfolios.

- Total International Market (VXUS or FTIHX) — Every publicly traded company outside the U.S. Diversification beyond America.

- U.S. Bond Market (BND or FXNAX) — Lower return, lower volatility. Useful for stability as you approach retirement.

You could build a complete, lifelong investment portfolio with just these three funds.

The Math That Changes Everything

$10,000 invested in a total market index fund in 1993 would be worth approximately $200,000+ today — a 20× return over 30 years, with no active management, no stock picking, and no expertise required.

The same $10,000 in a savings account earning 0.5%? About $16,000.

How to Actually Start

- Open a Roth IRA at Fidelity or Vanguard (free, takes 10 minutes)

- Contribute up to $7,500 for the year

- Buy FSKAX (Fidelity) or VTI (Vanguard)

- Set up automatic monthly contributions

- Don’t look at it during market dips — stay the course

The hardest part isn’t the math. It’s resisting the urge to panic when the market drops 20% and sell everything. The investors who get rich are the ones who keep buying during the dips.

Start today. Your future self will be grateful. Once you’re investing consistently, the next question becomes: how much do you actually need to retire early?