Real Estate Depreciation: The Tax Break Most Investors Never Use

By Marcus Webb | Aedilis

When I bought my first rental property, my accountant told me I’d have a $9,400 paper loss I could use to offset my income. I hadn’t lost any money. The property cash-flowed positive from day one. But the IRS lets you pretend it’s losing value — and that pretend loss is real on your tax return.

This is depreciation. And it’s one of the most powerful tax strategies available to real estate investors.

How Depreciation Works

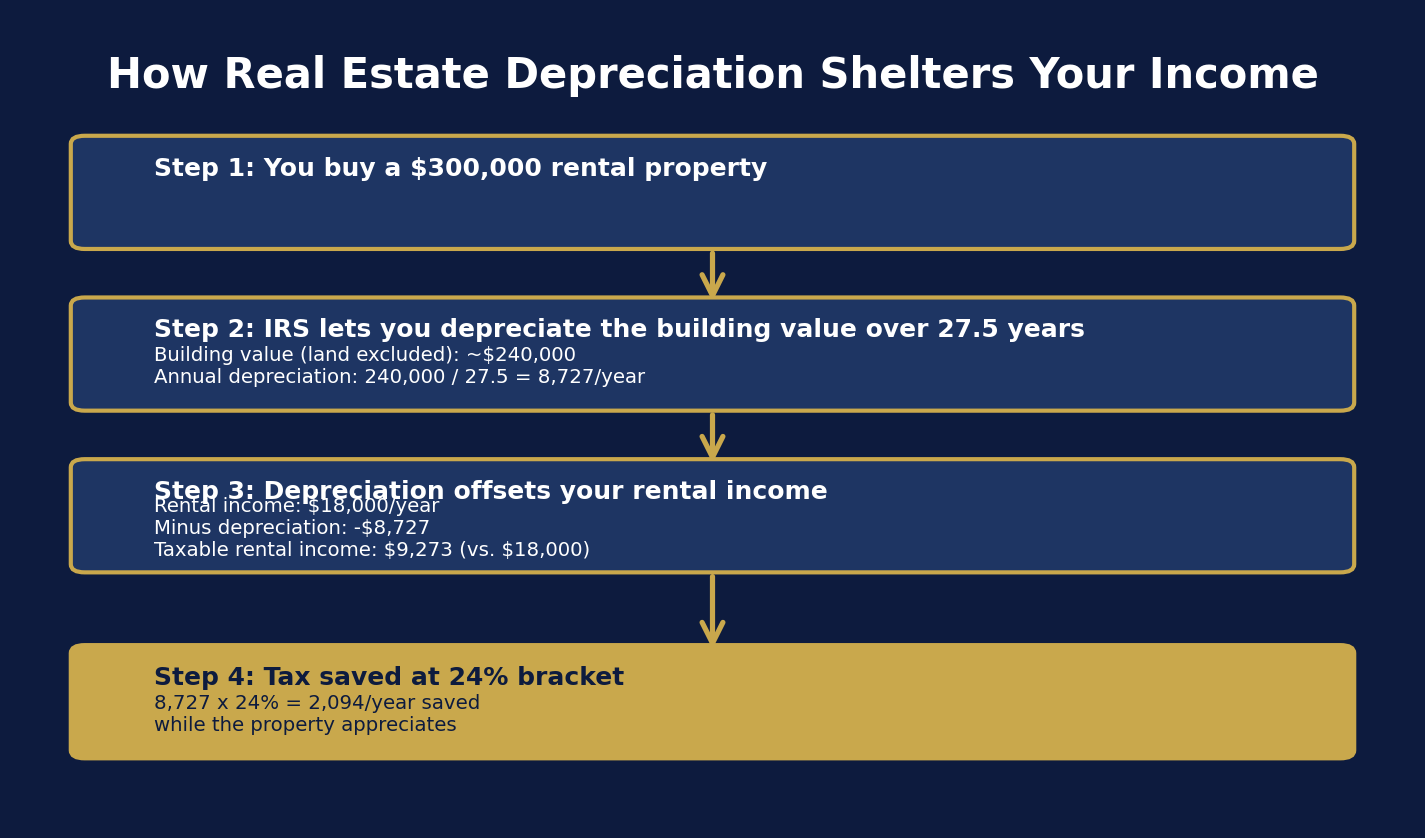

The IRS assumes residential rental property wears out over 27.5 years. So they let you deduct 1/27.5th of the building’s value every year as a “loss” — even if the property is actually appreciating.

Buy a $300,000 rental property. The land is worth $60,000 (land doesn’t depreciate). The building is worth $240,000. Divide by 27.5 years: you get an annual depreciation deduction of $8,727.

That $8,727 reduces your taxable income — even though you didn’t spend a single dollar. At a 24% tax bracket, that’s a $2,094 reduction in your tax bill every year, just for owning the property.

Depreciation by Property Value

- $200,000 property (80% building) → $5,818/year deduction

- $300,000 property → $8,727/year

- $500,000 property → $14,545/year

- $750,000 property → $21,818/year

Bonus Depreciation and Cost Segregation

Under recent tax law, you can accelerate depreciation significantly. A cost segregation study breaks a property into components — appliances, flooring, landscaping — that depreciate over 5-15 years instead of 27.5. This front-loads your deductions, giving you larger write-offs in the early years when they’re most valuable.

For a $500,000 property, a cost segregation study might generate $60,000-$100,000 in Year 1 deductions instead of $14,545. The study costs $3,000-$8,000 and typically pays for itself many times over.

The Real Estate Professional Status Unlock

Normally, rental losses can only offset other passive income (other rental income). But if you or your spouse qualifies as a Real Estate Professional — defined as spending more than 750 hours per year on real estate activities — those losses can offset W2 income directly.

A doctor earning $400,000/year with a qualifying spouse who manages properties could shelter substantial W2 income with real estate depreciation. This is legal. This is the tax strategy that wealthy people use.

Depreciation Recapture: The Trade-off

When you sell, the IRS recaptures depreciation at a maximum 25% rate. But if you use a 1031 exchange — rolling proceeds into a new property — you defer both capital gains and depreciation recapture indefinitely.

Own properties for life, do 1031 exchanges, and pass them to heirs who get a stepped-up cost basis: your heirs never pay the deferred taxes. The depreciation was effectively free.

This is why real estate is the cornerstone of generational wealth. The depreciation deduction alone is worth understanding — even if you own just one rental property. New to this and earning a W2 paycheck? Start with how to start real estate investing on a W2 salary.

One Comment