How to Pay Less Taxes as a W2 Employee (Legally)

⚡ Key Takeaways: Paying Less Taxes as a W2 Employee

- W2 employees have fewer tax levers than business owners — but the levers that exist are powerful and underused.

- Your 401(k) is your biggest single tool: contributing $24,500 saves ~$5,170 in taxes at the 22% bracket in the same year you contribute.

- An HSA is a triple tax advantage — deductible contributions, tax-free growth, tax-free withdrawals for medical expenses.

- The Backdoor Roth IRA is a legal workaround for high earners who earn above the Roth IRA income limit.

- Tax-loss harvesting, FSAs, and dependent care accounts are additional tools most W2 employees never use.

🆕 2026 Legislative Updates: The OBBBA added new tax breaks on top of these strategies: deduct up to $12,500 of overtime premium pay, tipped workers can deduct up to $25,000 in tip income, and 401(k) limits rose to $24,500 with a new super catch-up for ages 60–63.

By Maya Chen | Aedilis

I sat down with my W2 that year and stared at the number in Box 2: Federal income tax withheld. I knew I’d had a decent year. But that number — the amount I’d sent to the government — felt enormous. And I thought: is this right?

Turns out, it wasn’t. Not wrong in an illegal sense — I’d paid exactly what I owed based on how I was structured. The problem was how I was structured. I wasn’t taking advantage of a single legal tax reduction strategy available to W2 employees. I was just earning money and watching it get taken.

That changed. And now I want to show you what I learned.

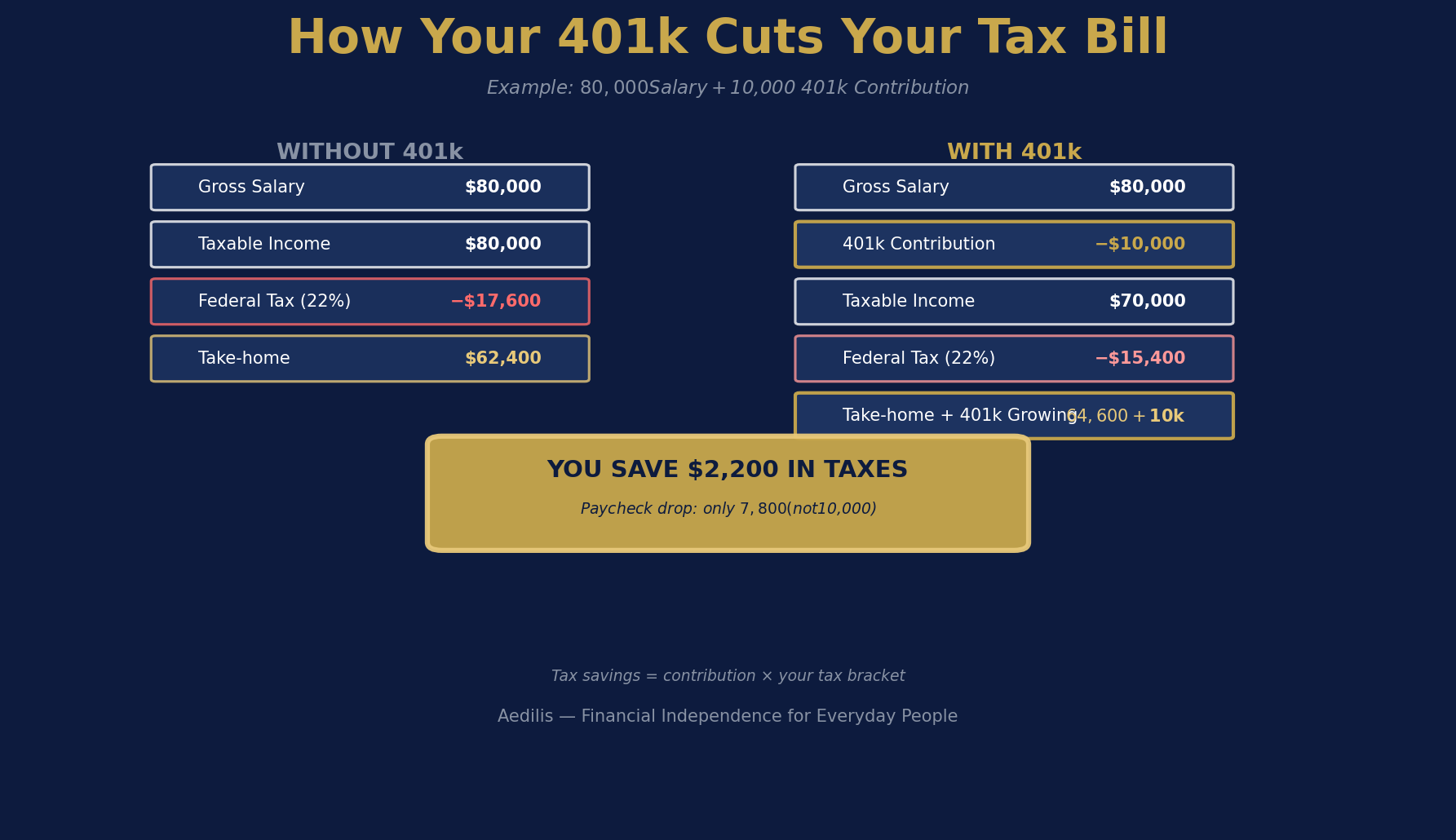

The 401(k): Your Biggest Lever

Contribute $24,500 in 2026, and you only pay income tax on the money that’s left. At a $80,000 salary, that’s $56,500 in taxable income. At the 22% bracket, that’s a $5,170 tax reduction — immediately, that year.

Max it every year. The match is free money. The tax break is immediate and substantial.

The HSA: Triple Tax Protection

If you’re on a high-deductible health plan, you qualify for an HSA. The 2026 limits are $4,300 (individual) or $8,550 (family). Contributions are pre-tax, growth is tax-free, and withdrawals for medical expenses are tax-free.

Invest your HSA in index funds and let it compound. At 65, you can withdraw for any reason (you pay ordinary income tax, like a Traditional IRA). It’s a stealth retirement account. For a deeper breakdown, see The HSA: The Only Account With Three Tax Breaks.

The FSA: Use It or Lose It — But Use It

A Flexible Spending Account (FSA) lets you set aside up to $3,300 in 2026 pre-tax for medical or dependent care expenses. Unlike an HSA, you don’t need a high-deductible plan. The catch: it’s use-it-or-lose-it. But if you have predictable medical costs, it’s free money.

Charitable Contributions

If you give to charity, do it with appreciated stock rather than cash. You avoid capital gains tax on the appreciation and deduct the full fair market value — two tax wins from one donation. In low-income or early-retirement years, you may also qualify for the 0% federal capital gains rate, turning those gains entirely tax-free.

Commuter Benefits

Up to $325/month in transit or parking costs can be set aside pre-tax through employer commuter benefit programs in 2026. If you commute, this is free money you may be leaving on the table.

The Backdoor Roth: For High Earners

Above $150,000 (single) or $236,000 (married) in 2026, you can’t contribute directly to a Roth IRA. The backdoor Roth fixes this: contribute to a Traditional IRA, then convert it immediately. The conversion is taxable only on gains (which are minimal if you convert quickly), and then the money grows tax-free forever.

Start a Side Business

Even a small side business opens legitimate deductions: home office, equipment, software, a portion of your phone and internet. The government wants to encourage entrepreneurship — these deductions are the incentive.

The pattern is clear: the tax code rewards people who plan. Every strategy here is legal, common, and available to any W2 employee. The question is whether you use them.

Frequently Asked Questions: W2 Employee Taxes

Can W2 employees really reduce their taxes, or is that only for business owners?

W2 employees have fewer options than business owners, but the tools that exist are significant. Maxing a 401(k), HSA, and using a Backdoor Roth IRA can reduce your taxable income by $30,000 or more per year — that’s a real tax bill reduction of $6,000–$10,000 annually depending on your bracket. The difference is that business owners can deduct operating expenses, which W2 employees cannot.

What is the Backdoor Roth IRA and who should use it?

The Backdoor Roth IRA is a legal two-step workaround for high earners who exceed the Roth IRA income limits ($161,000 single / $240,000 married in 2024). You contribute to a Traditional IRA (no deduction at high incomes), then immediately convert it to a Roth IRA. The result: Roth benefits regardless of income. Anyone earning above the direct Roth income limit should consider it.

Is contributing to a 401(k) always worth it, even if my investments underperform?

Yes — the tax break alone makes it worth it even before considering returns. If you’re in the 22% bracket and contribute $5,000 to a 401(k), you save $1,100 in taxes immediately. That’s an instant 22% return before your investments grow a dollar. The compound tax advantage over 20–30 years is enormous.

What is tax-loss harvesting and can W2 employees use it?

Tax-loss harvesting is selling investments that have declined in value to realize a loss, which offsets capital gains taxes or up to $3,000 of ordinary income per year. Yes, W2 employees with taxable brokerage accounts can use it. It’s most effective during market downturns and requires holding replacement investments to maintain your market exposure.

How much can I save in taxes as a W2 employee if I implement all these strategies?

It depends on your income and situation, but a W2 employee earning $100,000 who maxes their 401(k) ($24,500), HSA ($4,300 single), and uses a Backdoor Roth could reduce their taxable income by $27,800. At the 22% bracket, that’s roughly $6,116 in tax savings per year — and potentially $150,000+ over a 25-year career.

One Comment