The 529 Plan: How to Save for College AND Cut Your State Tax Bill

By Maya Chen | Aedilis

When people think about college savings, they usually think about putting money away and hoping it grows. The 529 plan does that — but it also does something most people don’t realize: in most states, it cuts your state taxes right now, this year, while you’re saving.

That combination — current tax break plus tax-free growth — makes the 529 one of the most underused financial tools available to parents.

How the 529 Works

A 529 is a state-sponsored college savings account. You contribute after-tax dollars, the money grows tax-free, and withdrawals for qualified education expenses (tuition, room and board, books, computers) are completely tax-free.

Unlike a Roth IRA, there’s no annual contribution limit set by the IRS — you can contribute as much as you want, subject to gift tax rules (up to $19,000/year per child without triggering gift tax in 2026, or $95,000 via 5-year superfunding).

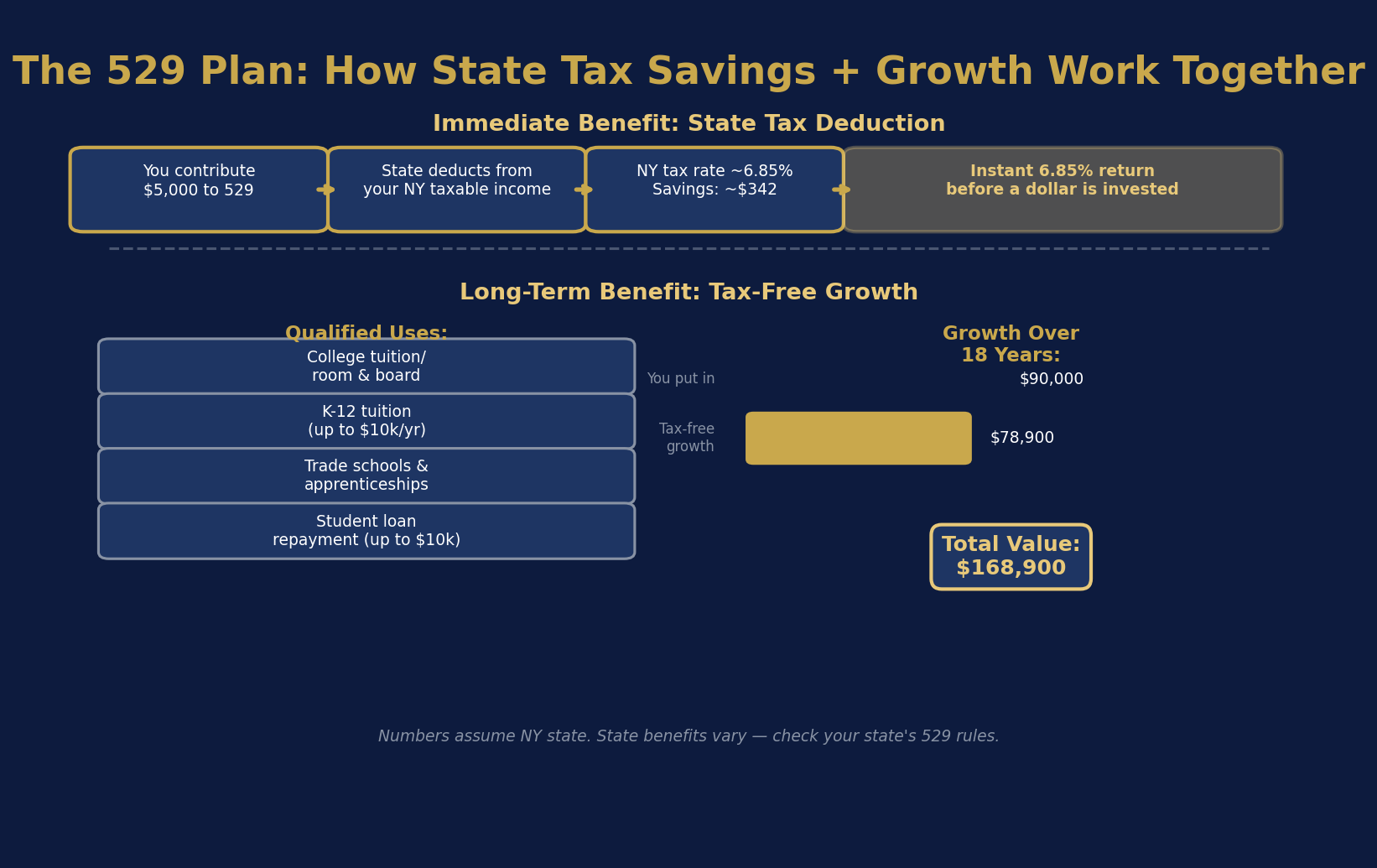

The State Tax Deduction (The Underrated Part)

34 states offer a state income tax deduction for 529 contributions. If you live in one of these states, every dollar you contribute reduces your state taxable income.

New York example: NY offers a deduction of up to $5,000/year (single) or $10,000/year (married). At a 6.85% state tax rate, a married couple contributing $10,000 saves $685 in state taxes that year. Every year you contribute. That’s not the investment growth — that’s just the tax break for making the contribution.

Some states (like Indiana, Utah, Vermont) offer direct tax credits — even better than deductions. Check your state’s rules.

The Growth Math

$5,000/year for 18 years at 7% average return = approximately $168,900. Your total contributions: $90,000. Tax-free growth: $78,900 — which you’d otherwise pay capital gains tax on.

SECURE 2.0: The Roth Rollover Safety Net (2024+)

One of the biggest fears with 529 plans was: what if my kid doesn’t go to college? Starting in 2024, unused 529 funds can be rolled over to the beneficiary’s Roth IRA — up to $35,000 lifetime, subject to annual Roth IRA limits, and the account must be at least 15 years old.

This removed the biggest downside of 529 plans. If your child gets a scholarship or doesn’t need the money for college, the funds can convert to a retirement head start instead of being penalized.

Superfunding: The Lump-Sum Option

You can contribute up to 5 years’ worth of annual gift exclusions at once — $95,000 per child in 2026 — and treat it as if you contributed it over five years for gift tax purposes. If you receive an inheritance or have a windfall, superfunding a 529 early maximizes the compound growth timeline.

Open the account when the child is born. Contribute consistently. Invest in age-based index fund portfolios that automatically shift from growth to conservative as college approaches. The 529 is one of the simplest wealth-building tools available to families — and one of the most ignored. And if a 529 ends up overfunded, 2026 rules let you roll up to $35,000 of leftover funds into the beneficiary’s Roth IRA — see the 529-to-Roth IRA rollover guide for 2026. New parents should also weigh the new Trump Account — the $1,000-seeded investing account for kids — alongside the 529.