How to Prioritize Your Investments: The Order of Operations That Actually Makes Sense

By Jamie Park | Aedilis

When I first got serious about investing, I made the classic mistake: I started putting money in random places without a strategy. A little in my 401k, some in a savings account, a bit in individual stocks. I felt like I was doing something, but I had no idea if I was doing it right.

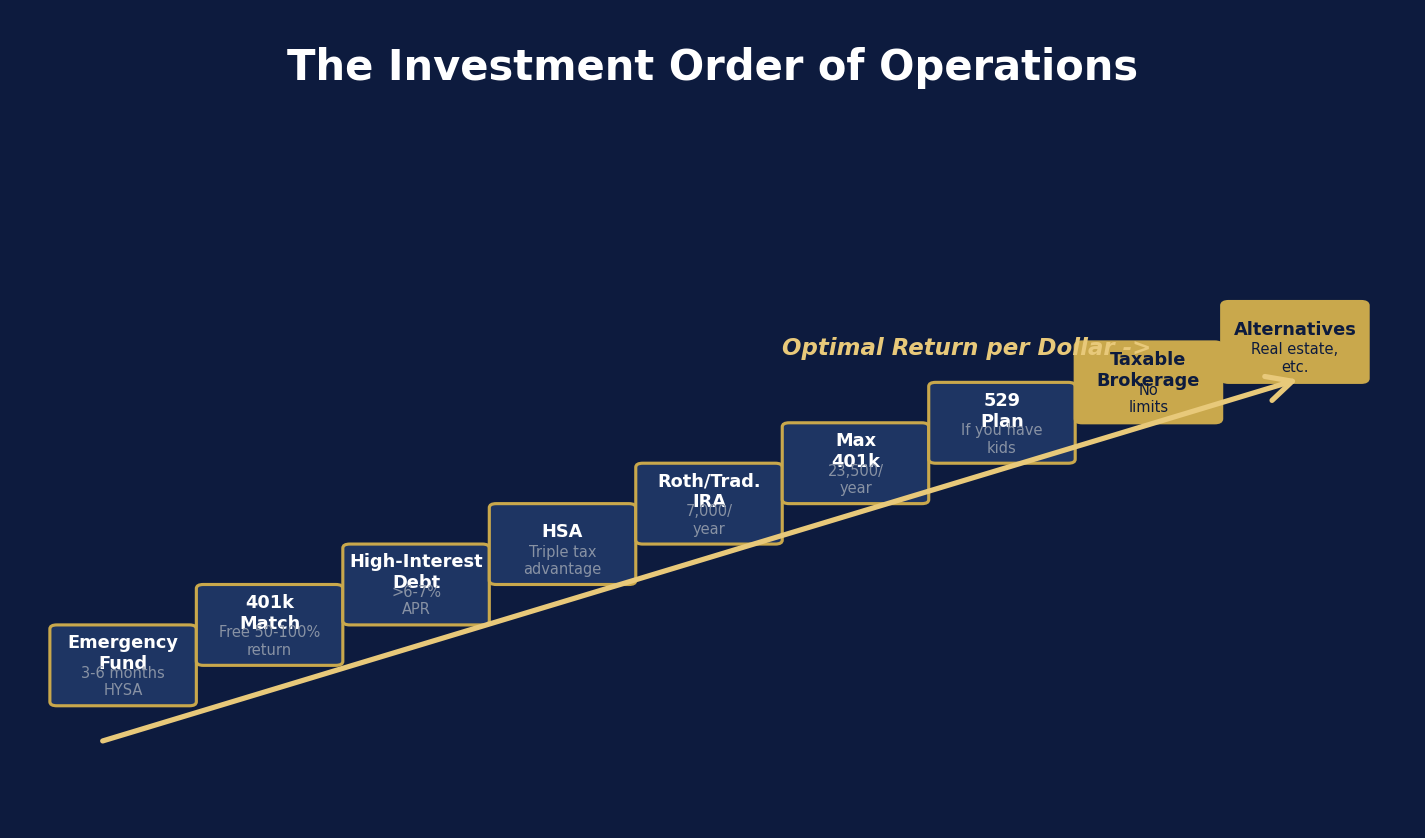

The answer — which I eventually found — is called the investment order of operations. Do these steps in this order, and you’ll never have to wonder if you’re making the right move.

Step 1: Emergency Fund (1-3 months expenses)

Before anything else. If you have no emergency fund and something breaks, you’ll raid your investments at the worst time. Keep 1-3 months of expenses in a high-yield savings account — enough to handle surprises without touching your investments.

Step 2: Employer 401k Match (100% return)

Contribute exactly enough to get your full employer match. If your company matches 3%, contribute 3%. This is a 100% guaranteed immediate return. Nothing in investing beats it. Do this before anything else.

Step 3: High-Interest Debt

Credit cards at 18-25%? Pay them off. No investment reliably beats 18% guaranteed. Every dollar of credit card debt paid is like earning 18-25% tax-free.

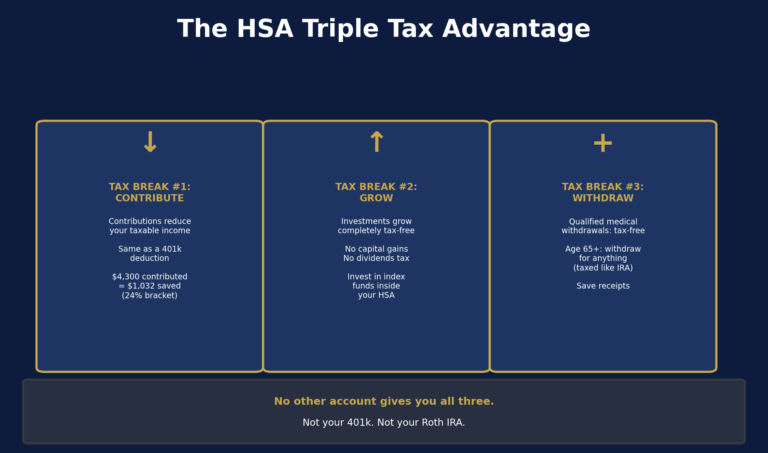

Step 4: HSA (if eligible)

If you have a high-deductible health plan, max your HSA before your IRA. It’s the only triple-tax-advantaged account that exists. 2026 limits: $4,300 individual / $8,550 family.

Step 5: Roth or Traditional IRA ($7,500/year)

Choose Roth if you’re in a lower tax bracket now (under ~$75k single / $150k married). Choose Traditional if you’re in a higher bracket and expect lower income in retirement. Max it every year. Earning too much to contribute to a Roth IRA directly? The backdoor Roth IRA is how high earners still get in. (Planning to retire early? The Roth conversion ladder is how you access this money before 59½ without penalties.)

Step 6: Max 401k ($24,500 in 2026)

After the match and IRA, go back and max your 401k to the full limit. This reduces your taxable income significantly and sets you up for compound growth over decades.

Step 7: 529 for Kids’ College (if applicable)

If you have children, a 529 plan gives you state tax deductions on contributions and tax-free growth for education expenses. Most states offer deductions on contributions.

Step 8: Taxable Brokerage Account

Once all tax-advantaged accounts are maxed, invest in a regular brokerage account. Use index funds, hold long-term, and manage for tax efficiency (hold broad funds that generate minimal dividends).

Step 9: Real Estate and Alternatives

With a solid foundation built, consider real estate for cash flow and depreciation benefits, or REITs for real estate exposure without direct ownership.

The order matters because each step has diminishing returns once the one above it is maximized. The employer match is the highest guaranteed return you’ll ever find. The HSA beats the IRA because of the extra tax advantage. Work down the list — and once something is maxed, move to the next step.