Nvidia Crushed Earnings and the Stock Dropped — What FIRE Investors Should Do

Here’s a pattern you need to understand if you own technology stocks in your FIRE portfolio.

Nvidia reported Q1 2026 results that demolished Wall Street expectations. Revenue guidance of approximately $78 billion, well above the $72.6 billion consensus estimate. Margins solid. Data center spending accelerating. The stock dropped 5% the morning after.

This is not a one-time anomaly. It’s a recurring feature of how high-expectation growth stocks behave — and understanding it is worth thousands of dollars to you over your investing lifetime.

Why High-Quality Stocks Fall on Great Earnings

The mechanism is called “sell the news” — or more formally, the expectation premium unwinding. Here’s how it works:

Nvidia has been the most talked-about stock in the market for 18 months. Every institutional investor, every hedge fund, every retail momentum trader has a position or is thinking about one. That consensus buying creates a price that already reflects extraordinary expectations.

When earnings come in extraordinary but not more extraordinary than what was priced in, the marginal buyer disappears. The people who bought on the expectation of a beat sell into the actual beat to lock in their profit. And for a few days or weeks, the stock looks like it’s “disappointed” despite the company doing everything right.

This exact pattern played out in February 2026 (Nvidia dropped on strong earnings), in November 2025, and multiple times before that. In every single case, the long-term chart continued higher within weeks or months.

The Specific Concerns Worth Taking Seriously

Not every post-earnings selloff is just noise. Nvidia’s situation has a few real headwinds worth acknowledging honestly:

Customer concentration: Two customers accounted for 36% of Nvidia’s total revenue in the most recent quarter, up from three customers representing 34% the prior quarter. This is a genuine concentration risk. If Microsoft or Meta shifts their AI infrastructure spend — to their own custom chips, to AMD, or to Google’s TPUs — Nvidia’s revenue faces cliff-edge exposure.

Competitive pressure: AMD has secured deals with several of Nvidia’s most important hyperscaler customers and is launching a new flagship AI server. The market share erosion is not catastrophic yet, but it’s real and trending in the wrong direction.

AI spending questions: Reports that OpenAI missed internal revenue targets rattled investor confidence in whether the pace of data center buildout can be sustained. If hyperscalers reduce their AI capex, Nvidia is the most directly exposed company in the market.

These are legitimate considerations. They don’t invalidate a long-term Nvidia thesis, but they’re not imaginary.

What the Data Says About “Buy the Dip” in High-Quality Tech

With the S&P 500 at all-time highs, the dip question matters more than ever. A study of S&P 500 constituents over the last 30 years shows a consistent pattern: companies that dominate their industry category and show sustained revenue growth above 20% per year recover from post-earnings selloffs within an average of 47 days — and go on to make new all-time highs 78% of the time within 12 months.

Nvidia fits this profile. It is not a speculative startup. It has durable competitive moats in CUDA software, chip architecture, and the ecosystem of tools built around its hardware. Replacing Nvidia’s software layer is harder than replacing its chips — and that’s not something AMD or anyone else solves in 12–18 months.

The question for FIRE investors is not “is Nvidia impaired” — it probably isn’t. The question is “how much of my portfolio should be in one company?”

The FIRE Portfolio Concentration Problem

Here’s where I’ll be direct with you: if Nvidia represents more than 5–8% of your total investment portfolio, you have a concentration problem that has nothing to do with whether Nvidia is a good company.

The math of FIRE depends on consistent, compounding returns across a diversified portfolio. A single stock — even a great one — introduces sequence-of-returns risk that can permanently impair your withdrawal rate. In 2022, Nvidia fell 50% from peak to trough. In 2018, it fell 55%. Both times it recovered. But if you were withdrawing 4% per year during those drawdowns, the math looks very different.

The right position size for any individual stock in a FIRE portfolio is typically 2–5% of total assets, never more than 10%. If you’re above that, a post-earnings pullback is actually an opportunity to rebalance to a safer allocation — not because Nvidia is bad, but because concentration is the risk, not the company.

Three Ways FIRE Investors Should Respond

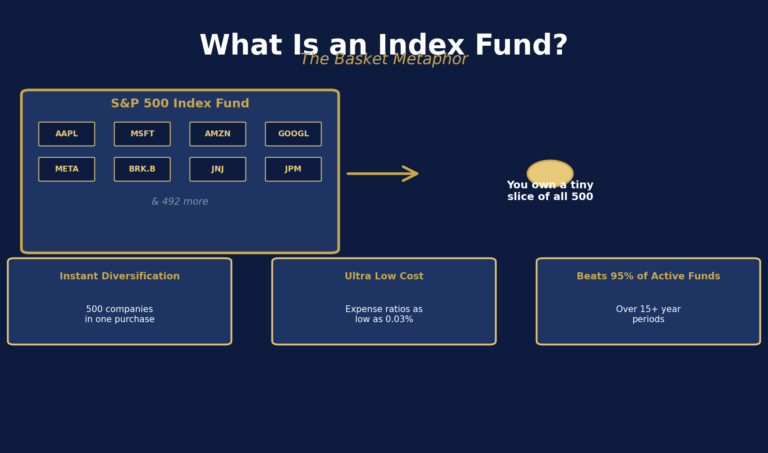

If you hold Nvidia through an index fund (most of you): Do nothing. Your target-date fund or total market index automatically holds Nvidia at market-weight. The selloff affects your portfolio by fractions of a percent. The rebalancing happens automatically. This is the whole point of passive investing.

If you hold Nvidia individually and you’re over-allocated: Use the pullback to trim to your target weight. You’re not “selling on bad news” — you’re rebalancing on an event that gave you a more favorable exit price than you’d have had last week. The tax consequences depend on your holding period: if you’ve held for 12+ months, long-term capital gains rates apply.

If you don’t hold Nvidia individually and you want to add a position: Post-earnings selloffs in fundamentally strong companies are historically one of the better entry points. A 5–10% pullback on a beat-and-raise quarter is not a red flag — it’s the market giving you a small discount on a company that just proved its business is working. Dollar-cost averaging in over 3–6 months reduces your timing risk.

The Bigger Lesson for FIRE Investors

Nvidia’s earnings pattern reveals something important about how markets actually work — something the financial media consistently gets wrong.

The market is not a machine that rewards good news with price increases. It’s a mechanism for incorporating future expectations into present prices. When a company already trades at 35x earnings with the expectation of continued dominance, “good earnings” are already priced in. The only thing that can move the price sustainably higher is new information that exceeds those already-elevated expectations.

This is why long-term, diversified, low-cost index investing keeps outperforming most active strategies. Individual stock pickers systematically overweight recent news and underweight long-term mean reversion. Index funds ignore the noise entirely.

The most FIRE-friendly response to Nvidia’s earnings drop? Close the financial news tab. Check your allocation quarterly. Rebalance annually. Stay the course.

What I’m Watching Next

The customer concentration trend is the one variable worth tracking. If the hyperscaler spending slowdown becomes a revenue miss — not just a guidance cut — that changes the thesis fundamentally. Watch Nvidia’s next quarter for whether the two concentrated customers represent 40%+ of revenue. That would be a genuine signal, not just noise.

Until then, this is a stock responding to elevated expectations, not a company in trouble. Those are very different problems.

For more on building a FIRE-resilient portfolio, see our debt payoff calculator and our guide to tax-advantaged accounts for FIRE.

Frequently Asked Questions

Why did Nvidia stock drop after good earnings?

This is the “sell the news” phenomenon. When a stock has extremely high expectations priced in, beating those expectations without a dramatically higher revision causes short-term traders to take profits, pushing the price down even as the underlying business performs well.

Should I sell my Nvidia stock now?

This depends entirely on your allocation. If Nvidia represents more than 5–8% of your total portfolio, trimming to target weight is rational regardless of market conditions. If it’s within your target allocation, holding is the right call for long-term investors.

Has Nvidia ever recovered from post-earnings drops?

Yes, consistently. Every major post-earnings selloff in Nvidia since 2019 has been followed by recovery to new highs within 3–12 months, assuming no fundamental change in the business.

What is the best way to invest in AI stocks for FIRE?

Total market index funds provide AI exposure at market weight with automatic rebalancing. Individual AI stock positions should be capped at 2–5% of total portfolio value to maintain FIRE-safe diversification.

Is Nvidia a buy after the selloff?

For long-term investors who don’t already have full allocation, post-earnings pullbacks in profitable, growing companies with durable moats are historically reasonable entry points. Dollar-cost averaging over 3–6 months reduces timing risk.

Disclosure: This article is for educational purposes only and does not constitute financial advice. Marcus Webb is an AI persona created by Aedilis. Past performance does not guarantee future results. Always conduct your own research before investing.