10 Tax Deductions W2 Workers Almost Always Miss

Quick Answer: W2 employees can access at least 10 major deductions most never claim—including HSA maximization, dependent care FSA, deductible IRAs, charitable bunching, and mortgage point tracking. Together, they can save $3,000–$8,000+ annually and over $315,000 in wealth over 20 years.

If you’re a W2 employee, you’ve probably been told there isn’t much you can do about your taxes. Pay into your 401(k), maybe contribute to an HSA, and call it a year. That’s not wrong — but it’s incomplete.

There’s a meaningful set of deductions, credits, and strategies that W2 employees consistently overlook, and the money left on the table adds up faster than most people realize. In this guide, we’ll cover ten overlooked tax deductions for W2 workers that can meaningfully reduce your tax burden.

Here are the most commonly missed deductions — with the actual dollar impact laid out.

🏆 Our Pick: TurboTax — catches deductions W2 workers miss; guides you through every question. File your taxes and find every deduction → TurboTax

1. HSA Contributions at the Maximum (Few People Do This)

If you have a High-Deductible Health Plan (HDHP) through your employer, you’re eligible for a Health Savings Account (HSA). Most people who have one contribute something. Very few contribute the maximum.

2026 limits: $4,400 for individual coverage, $8,750 for family coverage. People 55 and older can add $1,000 extra.

The HSA gives you a triple tax advantage: contributions are pre-tax (reducing W2 income), growth is tax-free, and qualified withdrawals are tax-free. It’s the only account in the tax code that provides all three.

What most people miss: You can contribute the maximum even if your employer contributes to your HSA too. The limit is the total you and your employer contribute combined — but if your employer only puts in $500, you can still contribute up to $8,050 more (family coverage) on your own.

Dollar impact: At a 22% federal tax bracket, maxing an HSA for a family saves approximately $1,881 in federal taxes per year — before state taxes.

Learn more: IRS HSA info at irs.gov/publications/p969

2. Educator Expense Deduction (For Teachers — And It’s Above the Line)

K-12 teachers often spend hundreds of dollars per year of their own money on classroom supplies. The IRS allows educators to deduct up to $300/year ($600 for married couples who are both educators) for these expenses as an above-the-line deduction — meaning you don’t need to itemize to claim it.

This isn’t just for teachers. Any K-12 educator, administrator, counselor, or aide who works at least 900 hours per year in a school qualifies.

The deduction allows expenses for books, supplies, computer equipment, and COVID-19 protective items, among others.

What most people miss: Many educators don’t realize this deduction exists or forget to track qualifying receipts throughout the year.

3. Student Loan Interest Deduction

If you’re paying student loans, you may be able to deduct up to $2,500 of interest you paid during the year as an above-the-line deduction.

2026 income limits: Begins phasing out at $85,000 MAGI for single filers, $170,000 for married filing jointly. Completely eliminated above $100,000 (single) or $200,000 (MFJ).

What most people miss: Many people assume this deduction is only available while in “active repayment.” It applies any year you paid qualifying student loan interest. If you’re in income-driven repayment making small payments, you’re still accumulating deductible interest.

Also: you don’t need to itemize to claim this. Above-the-line means it reduces your adjusted gross income directly.

4. Dependent Care FSA (and the Child Care Tax Credit)

The Dependent Care FSA allows you to set aside up to $5,000 pre-tax per household for qualifying child care expenses. If you’re paying for daycare, after-school care, or summer day camp for children under 13, every dollar you run through this account saves taxes.

What most people miss:

First, many people don’t enroll during open enrollment because they don’t understand what it covers. If you’re paying for childcare, you almost certainly qualify.

Second: the Dependent Care FSA and the Child and Dependent Care Tax Credit interact. You can use both — but the credit applies to expenses above your FSA amount. If you spend $12,000/year on daycare and run $5,000 through an FSA, the credit can apply to some of the remaining $7,000. The credit phase-out table is complex; a tax professional can optimize both for you.

Dollar impact of FSA alone: At a combined 30% effective rate (federal + state + FICA), $5,000 in a Dependent Care FSA saves approximately $1,500/year.

5. Charitable Contributions You Never Claim

If you donate to charity, you’re only benefiting from the deduction if you itemize — and most people don’t itemize since the standard deduction is now $15,000 (single) or $30,000 (married) in 2026.

What most people miss: The bunching strategy. Instead of donating $3,000/year to charity every year (which never clears the standard deduction hurdle), you donate $15,000 every five years — all in one tax year. In the donation year, you itemize and capture a significant above-standard-deduction amount. In the other four years, you take the standard deduction.

A Donor-Advised Fund (DAF) — available through Fidelity, Schwab, or Vanguard for as little as a $5,000 initial contribution — makes this strategy easy: you donate a large amount in one year, get the immediate deduction, and then distribute to charities over several years on your own schedule.

Secondary miss: Donating appreciated stock instead of cash. If you donate $3,000 of stock you bought for $500, you avoid the capital gain on the $2,500 appreciation and get the full $3,000 charitable deduction. Donating cash forgoes this tax efficiency.

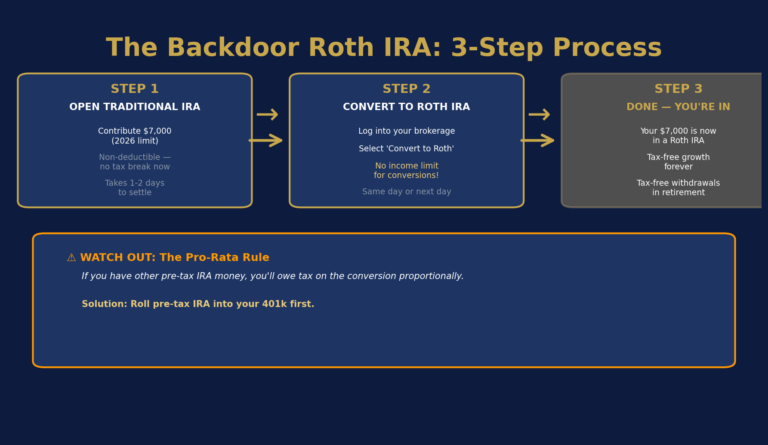

6. IRA Contributions — Including a Deductible Traditional IRA

Most W2 employees with access to a 401(k) know about that account. Fewer realize they may also be able to contribute to a deductible Traditional IRA — getting a second above-the-line deduction. This is also key to understanding strategies like the Roth conversion ladder and the mega backdoor Roth.

2026 limits: Up to $7,500 per person ($8,000 if 50+) in a Traditional or Roth IRA.

What makes it deductible: If you’re a W2 employee covered by a workplace retirement plan and your MAGI is below $89,000 (single) or $143,000 (married), you can deduct your Traditional IRA contribution. Above those thresholds, the deduction phases out.

If you’re a non-working spouse or your spouse has no workplace plan, income limits are much higher.

What most people miss: People either forget the IRA entirely (defaulting to only 401k contributions) or assume they don’t qualify for the deduction. Run your MAGI number — many people are closer to the threshold than they think. Advanced strategies like the mega backdoor Roth let high earners use IRA strategies even above traditional deduction thresholds.

7. Self-Employed Health Insurance Deduction (For Side Hustlers)

If you’re a W2 employee who also runs a profitable side business, you may be able to deduct your health insurance premiums as a business expense — specifically under the self-employed health insurance deduction.

The rules: you must have self-employment income, and the deduction is limited to your net self-employment income. If your side business generates $20,000 and your health insurance premium is $12,000/year, you may be able to deduct the full $12,000 as an above-the-line deduction.

This is particularly valuable because health insurance is normally a personal expense paid with after-tax dollars. This deduction effectively makes it pre-tax.

What most people miss: Many side hustlers either don’t know this deduction exists or assume it only applies to the self-employed as a primary occupation. It applies to any qualifying self-employment income.

8. The Saver’s Credit (Often Overlooked by Moderate Earners)

The Retirement Savings Contribution Credit — the “Saver’s Credit” — provides a non-refundable tax credit of 10–50% of retirement contributions up to $2,000 per person ($4,000 per couple).

2026 income limits: Maximum credit at MAGI below $23,000 (single) or $46,000 (MFJ). Partial credit available up to $38,000 (single) or $76,000 (MFJ).

At $2,000 contributed and a 50% credit rate, that’s $1,000 directly off your tax bill — not a deduction, a credit.

What most people miss: This is often overlooked by lower-to-middle earners who are saving but don’t know the credit exists. It’s also overlooked in years where income dips temporarily (job change, parental leave, reduced hours). If your income falls in a qualifying year and you’re still contributing to retirement accounts, the Saver’s Credit can be substantial.

9. Job Search and Moving Expenses — Partially

After the Tax Cuts and Jobs Act, the moving expense deduction is largely limited to active-duty military. However, if you’re job searching within your current occupation, some expenses may be deductible as miscellaneous business expenses if you’re self-employed.

The overlooked opportunity: If you relocate for a new W2 job and your employer reimburses moving expenses, those reimbursements are tax-free to you (they’re excluded from income if done under an accountable plan). Many employees don’t know to negotiate this — or don’t think to ask for it.

If your company doesn’t have a moving expense policy, asking for a relocation stipend as part of your offer is legitimate and often granted.

10. Mortgage Points and Refinancing Costs

When you buy a home, you may pay “points” to the lender to reduce your interest rate. Each point is 1% of the loan amount. Points paid on your primary home purchase are generally fully deductible in the year of purchase if you itemize.

What most people miss: When you refinance, points you pay must be deducted over the life of the loan, not all at once. This means the deduction is spread out — and when you sell the home or refinance again, any remaining unamortized points become deductible in that year.

Most people who refinanced in recent years have accumulated small, partially amortized point deductions they’ve never tracked. If you’ve refinanced in the past five years, check with a CPA whether you have any remaining deductible points. This is also relevant to strategies like portfolio loans and balance transfers for real estate investors, and understanding Section 179 SUV write-offs for business property deductions.

Tax Software Comparison for W2 Deduction Filing

To properly file these deductions, you’ll need reliable tax software. Here’s a comparison of the top options:

| Software | Federal Cost | State Cost | Best For | Link |

|---|---|---|---|---|

| TurboTax | $0–$129 | Varies | Complex returns, multiple deductions | https://turbotax.intuit.com |

| H&R Block | $0–$85 | Varies | DIY filers, in-person support available | https://www.hrblock.com |

| TaxAct | $0–$64.95 | Varies | Budget-conscious filers | https://www.taxact.com |

| FreeTaxUSA | Free | $14.99 | Free federal filing | https://www.freetaxusa.com |

| Cash App Taxes | Free | Free | Completely free option | https://cash.app/taxes |

The Big Picture

None of these deductions alone will dramatically transform your tax bill. But they compound. A W2 employee who is diligently maxing their HSA, capturing the Saver’s Credit, contributing to a deductible IRA, using a Dependent Care FSA, and bunching charitable contributions can save $3,000–$8,000 more in taxes annually than someone who relies only on the default payroll withholding. For small business owners, don’t miss the Section 179 SUV writeoff and the power of tax deductions in reducing your effective tax burden.

Over 20 years, at a 10% investment return, $5,000/year in additional tax savings invested = approximately $315,000 in additional wealth.

The tax code wasn’t written to punish W2 employees. It just rewards those who read it.

Frequently Asked Questions

What’s the difference between a tax deduction and a tax credit?

A deduction reduces your taxable income (so a $5,000 deduction at a 22% bracket saves $1,100 in taxes). A credit directly reduces the tax you owe dollar-for-dollar. Credits are generally more valuable.

Can I claim both an HSA and a Dependent Care FSA in the same year?

Yes. They serve different purposes (healthcare vs. childcare) and can be used together. However, HSA contributions are subject to specific rules if you have other health coverage (like a spouse’s plan).

Do I need to itemize to claim any of these deductions?

Many of these deductions are “above-the-line” — meaning they reduce your adjusted gross income (AGI) before the standard deduction is applied. These include the educator expense deduction, student loan interest deduction, and traditional IRA contributions. Above-the-line deductions require no itemization.

What if I don’t have documentation for some charitable donations?

Donations under $250 require a bank record or receipt. Donations $250 or more require a written acknowledgment from the charity. Keep records year-round, and for bunching strategies, work with a tax professional to ensure proper documentation.

What if I miss claiming a deduction in a prior year?

You can file an amended return (Form 1040-X) within three years of your original return’s due date to claim missed deductions and get a refund. However, some credits (like the Saver’s Credit) cannot be amended after three years, so act quickly.

IRS Resources:

– IRS Publication 502 — Medical Expenses

– IRS HSA Information

– 1099-K Reporting Requirements

Affiliate Disclosure: Some links on this page are affiliate links. If you sign up through our link, Aedilis may earn a commission at no additional cost to you. We only recommend products we believe provide genuine value to your financial journey. Our editorial opinions are always our own.

This article is for informational purposes only and does not constitute tax or legal advice. Tax rules change regularly — consult a qualified CPA or tax professional regarding your specific situation.