Your 401(k) Is a Tax Machine — Here’s How to Use It

By Maya Chen | Aedilis

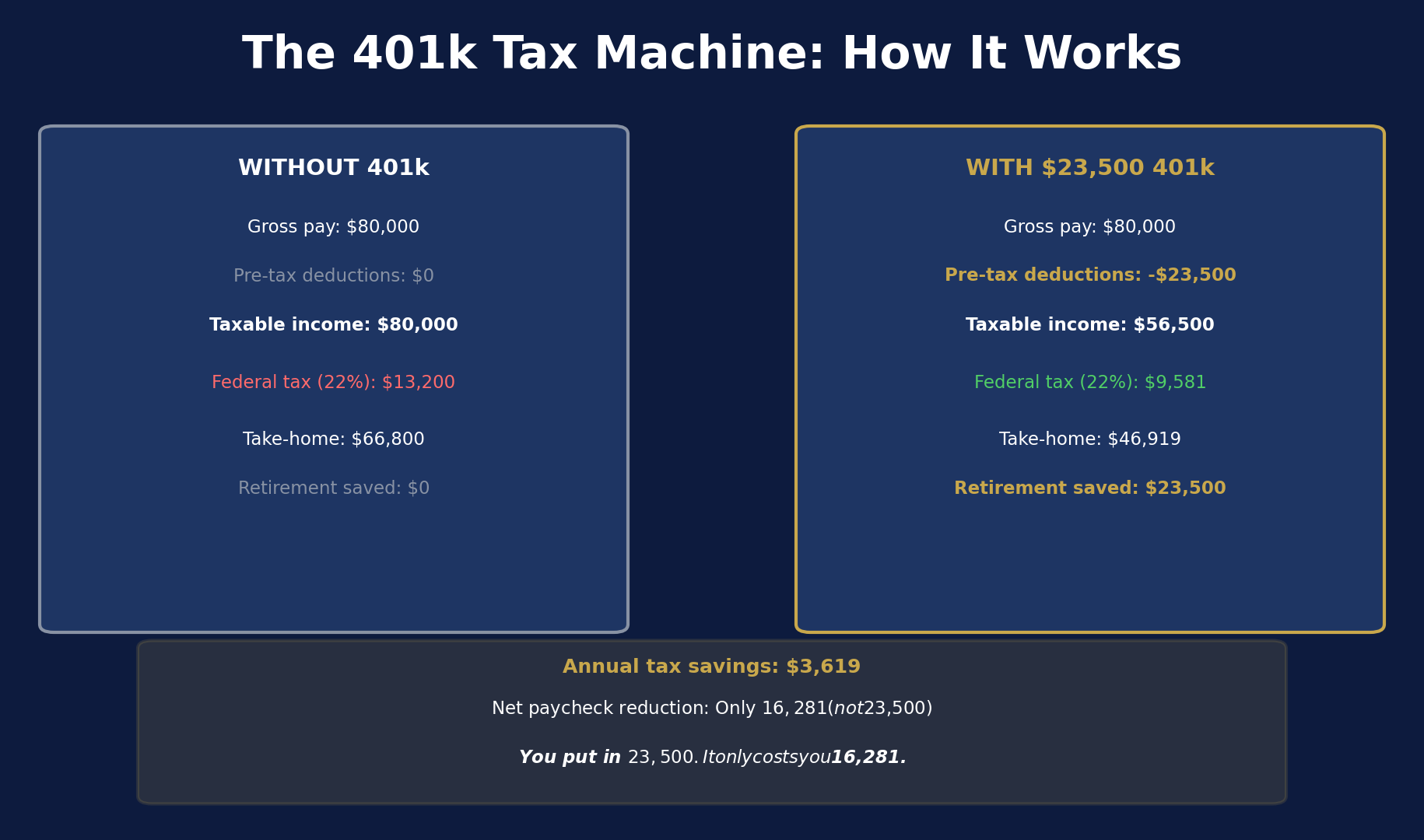

Most people treat their 401k like a savings account — put money in, hope it grows, retire someday. That’s not wrong, but it misses the most powerful part of what a 401k actually does: it reduces your taxes right now, this year, dramatically.

The Immediate Tax Math

Earn $80,000. Contribute $24,500 to your 401k. The IRS taxes you on $56,500 — not $80,000.

At the 22% federal bracket, that’s $5,170 less in federal income tax this year. Not a deduction you’ll see someday in retirement — money that doesn’t leave your paycheck right now.

Here’s the part that surprises people: contributing $24,500 doesn’t actually cost you $24,500 out of pocket. Because you save $5,170 in taxes (plus state taxes if applicable), the net cost to your take-home pay might be closer to $16,000-$18,000. You contributed $24,500 but only “felt” $16,000-$18,000 of it.

The 2026 Limits

- Under 50: $24,500/year

- 50-59 or 64+: $31,000 (catch-up contribution)

- 60-63: $34,750 (enhanced catch-up under SECURE 2.0)

- Employer match does NOT count toward your limit

Traditional vs. Roth 401k

Traditional 401k: Contributions are pre-tax. You pay taxes when you withdraw in retirement. Best if you’re in a higher tax bracket now than you expect to be in retirement.

Roth 401k: Contributions are after-tax. Growth and withdrawals in retirement are tax-free. Best if you’re in a lower bracket now or expect to be in a higher bracket in retirement. (Locked out of a Roth IRA by income? See the backdoor Roth IRA.) And if you’re over 50 and a high earner, the 2026 Roth catch-up rule now forces your catch-up contributions into Roth.

For most people in their 30s-40s in the 22% bracket, Traditional makes sense — you’re getting a tax break at 22% now, and you’ll likely be in a lower bracket in retirement.

The Long-Term Compounding

$24,500/year for 30 years at a 7% average annual return = approximately $2.35 million.

The same amount in a taxable brokerage account (with taxes on dividends and capital gains each year) would grow to approximately $1.8 million. The tax-deferred growth in the 401k adds roughly $550,000 over 30 years — just from avoiding annual taxation on growth.

The Employer Match: Never Leave It Behind

If your employer matches 3% of your salary, that’s $2,400/year on an $80k salary — completely free. No investment guarantees a 100% immediate return. Contributing at least enough to capture the full match is the single highest-ROI move in personal finance.

Start with the match. Then increase contributions by 1% each year at raise time. Within 5 years, you’ll be at or near the max without ever noticing the paycheck reduction. That’s the 401k working as a tax machine — quietly, automatically, compounding.