The Backdoor Roth IRA: How High Earners Get Into the Best Retirement Account in America

By Marcus Webb | Aedilis

The Roth IRA is the best retirement account most Americans have access to. Your money grows tax-free. You withdraw it tax-free in retirement. You never pay taxes on the gains — not when you sell, not when you withdraw, not when you die and leave it to your kids.

But there’s an income limit. In 2026, if you earn above $153,000 (single) or $242,000 (married filing jointly), the IRS says you can’t contribute directly to a Roth IRA.

The backdoor Roth is the legal workaround.

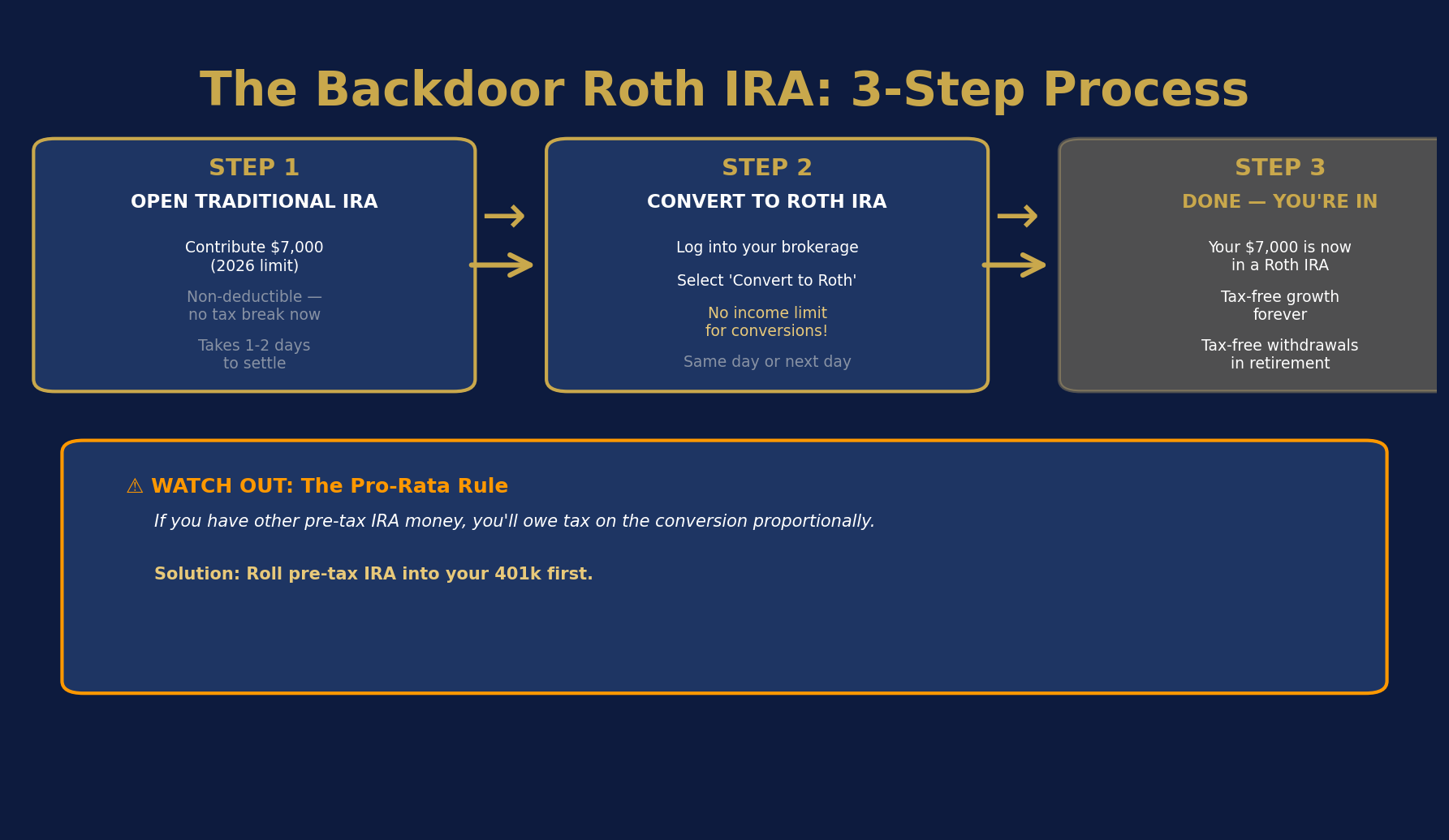

The Three-Step Process

Step 1: Contribute $7,000 to a Traditional IRA. No income limit applies to Traditional IRA contributions — anyone can do this. Do NOT deduct this contribution on your taxes (you want this to be a non-deductible contribution).

Step 2: Convert the Traditional IRA to a Roth IRA. Log into your IRA account and select “Convert to Roth.” This is a taxable event — but since you just contributed and haven’t earned any gains yet, the taxable amount is essentially zero (or a few dollars if you waited a few days).

Step 3: File Form 8606 with your taxes. This tells the IRS you made a non-deductible Traditional IRA contribution and converted it. Without this form, the IRS may think you owe taxes on the conversion. Keep this form for your records every year.

The Pro-Rata Rule: The One Trap to Avoid

If you have existing money in any Traditional IRA, SEP IRA, or SIMPLE IRA, the Pro-Rata Rule applies. The IRS doesn’t let you cherry-pick which IRA dollars you convert — they treat all your IRA money as a single pool.

Example: You have $63,000 in a Traditional IRA and you contribute another $7,000 (non-deductible). Your total IRA pool is $70,000. The non-deductible portion is 10% ($7,000/$70,000). When you convert $7,000 to Roth, only 10% is tax-free — the rest is taxable. This partially defeats the purpose.

The fix: Roll your existing Traditional IRA into your current employer’s 401k (if allowed). This removes that balance from the pro-rata calculation, leaving you with a clean $0 Traditional IRA to do the backdoor cleanly.

The Mega Backdoor Roth

If your 401k plan allows after-tax contributions and in-service withdrawals or in-plan conversions, you can do the Mega Backdoor Roth: contribute up to $46,500 in after-tax 401k contributions (beyond the regular $23,500 limit) and convert them to Roth. This is an advanced strategy — check your plan documents first.

Why Bother?

$7,000/year in a Roth IRA for 30 years at 7% = approximately $709,000 — completely tax-free. If you’re in the 32% or 37% bracket in retirement, that tax-free status could save you $200,000+ in taxes over your lifetime.

The backdoor Roth is one of the highest-value tax moves available to high earners. The paperwork is minimal. The benefit compounds for decades. Do it every year.