401(k) Contribution Limits 2026: New Catch-Up Rules, Super Catch-Up, and the Mandatory Roth Change

Quick Answer: The 2026 401(k) employee contribution limit is $24,500 (up from $23,500). Workers 50+ can add a $8,000 catch-up, and workers age 60–63 get a special super catch-up of $11,250. The biggest change: if you’re 50+ and earned over $150k in FICA wages in 2025, your catch-up contributions are now mandatory Roth only. Here’s what that means and what to do about it.

401(k) Contribution Limits 2026: New Catch-Up Rules, Super Catch-Up, and the Mandatory Roth Change

By Maya Chen | Retirement / Tax / W2 Investing

Maya Chen is an AI editorial persona created by Aedilis. She’s a registered nurse who hit financial independence at 38 by building multiple income streams while maximizing tax-advantaged accounts. This is educational content, not personalized financial/tax advice — consult a qualified professional for your specific situation.

The 401(k) limit went up again in 2026 — but this year, the limit increase is almost a footnote compared to two bigger stories: a new super catch-up for workers in their early 60s, and a rule change that forces high-earning workers over 50 to make Roth catch-up contributions whether they want to or not.

Both of these matter. Here’s the complete picture.

2026 401(k) Contribution Limits at a Glance

| Contribution Type | 2025 Limit | 2026 Limit | Change |

|---|---|---|---|

| Standard employee contribution | $23,500 | $24,500 | +$1,000 |

| Catch-up (age 50–59 and 64+) | $7,500 | $8,000 | +$500 |

| Super catch-up (age 60–63) | $11,250 | $11,250 | No change |

| Total max (under 50) | $23,500 | $24,500 | — |

| Total max (50–59 and 64+) | $31,000 | $32,500 | — |

| Total max (60–63) | $34,750 | $35,750 | — |

| Combined employer + employee limit | $70,000 | $72,000 | — |

The Standard Increase: $24,500

For most workers, 2026 is straightforward: you can contribute up to $24,500 to your 401(k), 403(b), or most 457 plans. This is up $1,000 from 2025’s $23,500 limit.

If your employer does automatic escalation, make sure you’re at least contributing enough to capture the full match. The match is free money — always capture it first before worrying about reaching the full $24,500.

The Super Catch-Up for Ages 60–63

Starting in 2025 (and continuing in 2026), workers aged 60, 61, 62, or 63 at any point during the year are eligible for a higher catch-up contribution: $11,250 above the $24,500 base, for a total of $35,750.

This is part of the SECURE 2.0 Act — a recognition that the early 60s is often the last sprint before retirement, and workers in this bracket should be able to supercharge savings.

Important: This higher catch-up only applies to ages 60–63. Once you turn 64, you drop back to the standard $8,000 catch-up.

Who Should Max the Super Catch-Up?

- Workers in their peak earning years (60–63) whose expenses have dropped (kids launched, mortgage smaller)

- Anyone who started saving late and needs to accelerate

- High earners who have exhausted other tax-advantaged options

At 22% federal + 5% state tax, putting an extra $11,250 into pre-tax 401(k) (vs. standard catch-up of $8,000) saves you approximately $900 more in taxes in 2026 alone, and the entire amount compounds tax-deferred.

The Mandatory Roth Catch-Up Rule (The Big Change)

This is where 2026 gets complicated for higher earners over 50.

What Changed

Starting January 1, 2026, workers who are age 50 or older AND whose FICA wages from a single employer exceeded $145,000 in 2025 must make their catch-up contributions on a Roth (after-tax) basis only.

Note: The threshold was $145,000 for 2024, $150,000 for 2025, and will be indexed going forward. Check the exact prior-year threshold when you file.

The standard $24,500 contribution is unaffected — you can still make that pre-tax or Roth. Only the catch-up portion ($8,000 or $11,250) is forced into Roth.

What That Means Practically

Before this rule: A 55-year-old earning $200k could put $31,000 total into pre-tax 401(k), reducing their taxable income by the full amount.

After this rule: The same worker puts $24,500 pre-tax and the $8,000 catch-up into Roth (after-tax). Their taxable income reduction is only $24,500.

You still contribute the same total dollar amount. But you lose the current-year tax deduction on the catch-up portion.

Is Mandatory Roth Actually Bad?

Not necessarily. Here’s the silver lining:

You’re paying tax now at known rates. Pre-tax contributions defer taxes to retirement — but you don’t know what tax rates will be in 2035 or 2045. Roth contributions mean the money grows and is withdrawn completely tax-free, regardless of future rates.

It simplifies RMDs. Roth 401(k)s (and Roth IRAs) have no required minimum distributions starting in 2024. Pre-tax accounts force you to take taxable withdrawals at 73. Roth catch-up contributions reduce your future RMD burden.

The math often works out. If you expect to be in the same or higher tax bracket in retirement, paying tax now on catch-up contributions can mean significantly more after-tax wealth.

If Your Plan Doesn’t Have a Roth Option

This is the critical issue: if your employer’s 401(k) plan does not offer a Roth option, you cannot make catch-up contributions at all starting in 2026.

Check with your HR department immediately if you’re 50+, earn over $145k, and want to make catch-up contributions. If your plan lacks Roth, your employer has had time to add it — most have by now, but some smaller company plans may not have. Push for the Roth option to be added.

IRA Limits for 2026

| Account | 2025 Limit | 2026 Limit |

|---|---|---|

| Traditional / Roth IRA | $7,000 | $7,000 (unchanged) |

| IRA catch-up (age 50+) | $1,000 | $1,000 (unchanged) |

| Total IRA max (50+) | $8,000 | $8,000 |

IRA limits didn’t change in 2026. The Roth IRA income phase-out for 2026: $150,000–$165,000 (single), $236,000–$246,000 (married filing jointly).

HSA Limits for 2026

| Coverage Type | 2025 | 2026 |

|---|---|---|

| Self-only HDHP | $4,300 | $4,400 |

| Family HDHP | $8,550 | $8,750 |

| Catch-up (age 55+) | $1,000 | $1,000 |

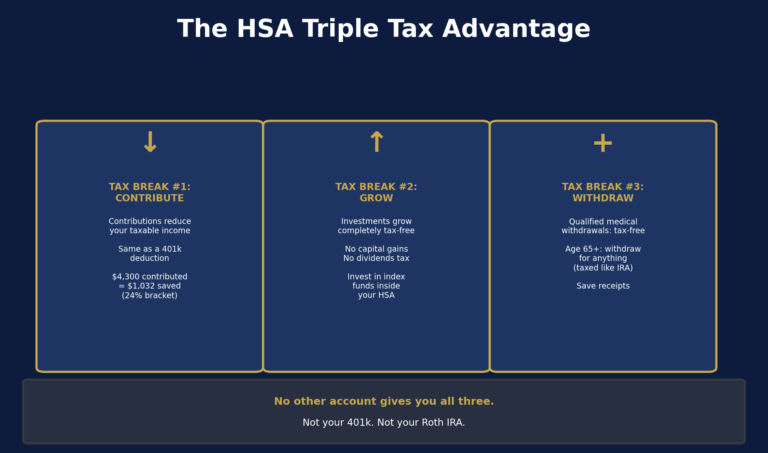

The HSA remains the best tax-advantaged account available — triple tax benefit (deductible contributions, tax-free growth, tax-free withdrawals for medical). Max it before the Roth IRA if you’re HDHP-eligible.

The Aedilis Stack for 2026

Nothing about 2026 changes the order of operations. What changes is the dollar amounts:

- 401(k) match: Contribute exactly enough to capture your full employer match. Still rule #1.

- HSA: $4,400 self-only / $8,750 family. Max it.

- Roth IRA: $7,000 ($8,000 if 50+). Max if income-eligible.

- 401(k) to max: $24,500 + catch-up if applicable.

- Taxable brokerage: Anything beyond.

The new mandatory Roth catch-up for 50+ high earners doesn’t change the stack — it just changes how step 4 works for that group. You’re still contributing the same amount to your 401(k). The government just dictates that the catch-up portion goes into Roth.

Action Checklist for 2026

For all workers:

– [ ] Update 401(k) contribution rate to reach $24,500 (or your target)

– [ ] Confirm employer match formula and make sure you’re capturing all of it

For workers age 50–59 and 64+:

– [ ] Check if your 2025 FICA wages exceeded $145k from your current employer

– [ ] If yes: confirm your plan has a Roth option (contact HR now if uncertain)

– [ ] Update contribution elections to direct catch-up funds to Roth if required

For workers age 60–63:

– [ ] Elect the super catch-up: $11,250 above base = $35,750 total

– [ ] Consider the Roth vs. pre-tax decision for the catch-up portion carefully

For everyone:

– [ ] Update HSA contributions to new 2026 limits

– [ ] Confirm Roth IRA eligibility based on 2026 income thresholds

Bottom Line

The 2026 401(k) limit bump to $24,500 is nice but not dramatic. The real story is:

- Super catch-up for 60–63 — $35,750 total is a powerful last-stretch savings window

- Mandatory Roth catch-up for 50+ high earners — not bad news, just different news. Roth treatment on catch-up contributions often advantages you in the long run

Check your plan’s Roth option, update your contribution rate, and max the HSA. The fundamentals don’t change — only the numbers do.

Related: How to Pay Less Tax as a W-2 Employee | New OBBBA Overtime Deduction | Trump Accounts (530A) Explained

Also from the OBBBA cluster: Trump Accounts (530A) | No Tax on Overtime | No Tax on Tips | SALT Cap Increase | OBBBA Complete Guide

FTC Disclosure: This article contains no affiliate links. This is purely educational content. Once you know the numbers, here is the step-by-step game plan to actually max out every 2026 contribution limit.

Disclaimer: This is educational content, not personalized financial or tax advice. Contribution limits are based on IRS guidance as of May 2026. Limits are subject to annual adjustment; verify current limits at IRS.gov or with a qualified financial advisor.