The HSA: The Only Account That Gets You Three Tax Breaks at Once

By Maya Chen | Aedilis

I ignored my HSA for two years. I thought it was just a way to pay for doctor’s visits with pre-tax dollars. Then my accountant explained what I was actually sitting on, and I felt like I’d been sleeping through the best class in school.

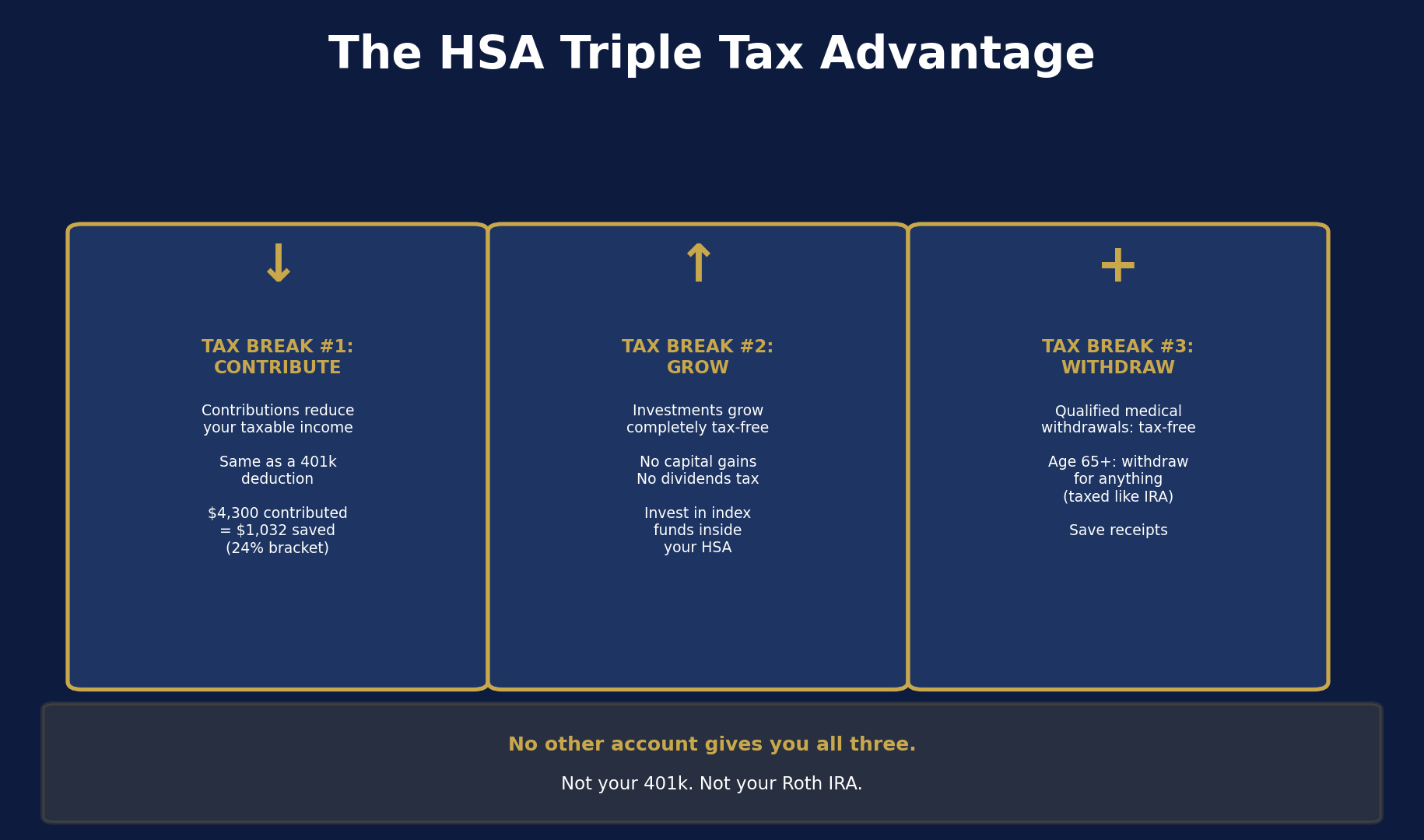

The HSA — Health Savings Account — is the only account in the U.S. tax code that gives you three separate tax advantages at the same time. No other account does this. Not your 401k. Not your Roth IRA. The HSA alone.

The Triple Tax Advantage

Tax break #1: Contributions are pre-tax. Every dollar you put into your HSA reduces your taxable income, just like a Traditional 401k. In 2026: $4,300 (individual) or $8,550 (family).

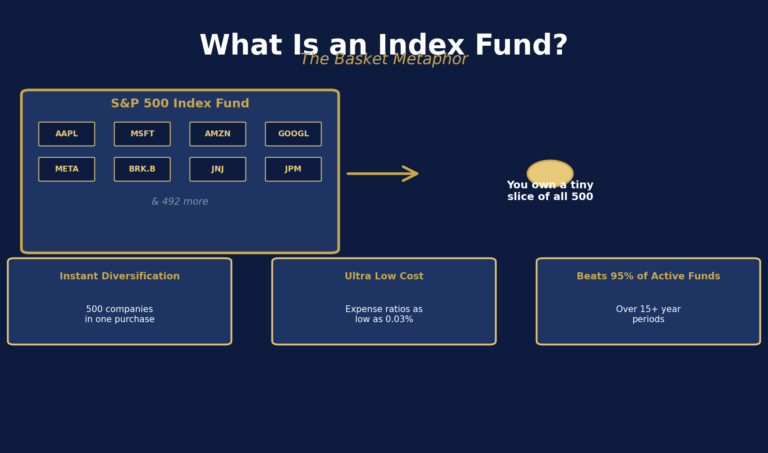

Tax break #2: Growth is tax-free. Invest your HSA in index funds and the gains are never taxed — not annually, not on withdrawal for qualified expenses.

Tax break #3: Withdrawals for medical expenses are tax-free. Unlike a Traditional IRA (where withdrawals are taxed), HSA withdrawals for qualified medical expenses are completely tax-free at any age.

That’s pre-tax in, tax-free growth, tax-free out — for an enormous category of expenses that everyone will eventually have.

The Stealth Retirement Account Strategy

Here’s the move most people miss: don’t spend your HSA. Pay your medical bills out of pocket today, save the receipts, and let your HSA compound in index funds for decades.

The IRS doesn’t put a time limit on reimbursement. You can submit a medical expense you paid in 2026 for tax-free reimbursement in 2046 — if you kept the receipt. That means every medical bill you pay out of pocket today is a future tax-free withdrawal you’ve pre-approved.

Meanwhile, your HSA balance grows at 7% annually. $4,300/year for 20 years at 7% = approximately $187,000. If you’ve accumulated $50,000+ in qualified medical expenses (easy to do over 20 years), you can withdraw $50,000 completely tax-free at any point.

After Age 65: A Second IRA

At 65, the HSA becomes a second Traditional IRA. You can withdraw for any reason — not just medical expenses. Non-medical withdrawals are taxed as ordinary income (same as a Traditional IRA), but there’s no penalty. The triple tax advantage still applies to all medical withdrawals.

Effectively: max your HSA, invest it in index funds, and you have a tax-advantaged account that converts to a Traditional IRA at 65 with zero downside.

The Requirement: High-Deductible Health Plan

To contribute to an HSA, you must be enrolled in an HDHP (High-Deductible Health Plan). In 2026, the minimum deductible is $1,650 (individual) or $3,300 (family).

Compare the premium savings of your HDHP vs. your low-deductible plan. In many cases, the premium savings alone more than cover the higher deductible — and you still get the triple tax advantage on top.

If you have access to an HSA and you’re not maxing it, you’re leaving three simultaneous tax breaks on the table. Start now.

2 Comments