7 Ways to Recession-Proof Your Finances in 2026 (The W2 Worker’s Playbook)

7 Ways to Recession-Proof Your Finances in 2026 (The W2 Worker’s Playbook)

This article may contain affiliate links. We may earn a commission at no cost to you. Our editorial opinions are never influenced by affiliate relationships.

Here’s what I wish someone had told me before every economic downturn I’ve lived through as a nurse: the people who come out ahead aren’t the ones who predicted it. They’re the ones who built the right foundations before it arrived.

Moody’s currently puts recession risk at around 30% for 2026 — down from 40% earlier this year, but still elevated enough that ignoring it is a choice, not a strategy. Tariff-driven inflation is running at 3.3%, CPI is at 3.8%, and 42% of Americans have no emergency fund at all. That last number is the one that keeps me up at night.

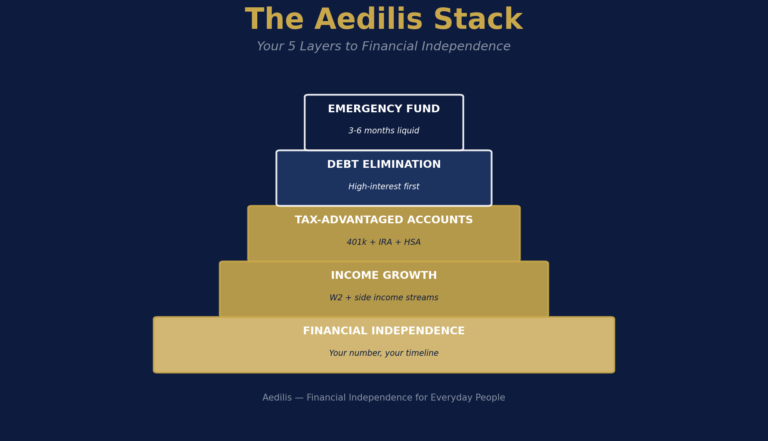

Here’s the thing nobody talks about: FIRE principles are recession principles. Bigger emergency fund. No consumer debt. Side income. Diversified accounts. If you’ve been building toward financial independence, you’re already ahead. If you haven’t started yet, now is the right time — not in spite of economic uncertainty, but because of it.

These are the 7 moves I’d make (and have made) right now.

Quick Summary: Build a 6–12 month emergency fund, eliminate high-interest debt, activate side income, keep your 401(k) running, capture available OBBBA tax savings, create a job-loss contingency plan, and recalibrate your FIRE timeline for persistent inflation.

1. Build a 6–12 Month Emergency Fund — Not the Old 3-Month Rule

The old “3 months of expenses” advice was written for a different economy. In a recession, job searches take longer, competition is stiffer, and opportunities are narrower. The math has changed.

Here’s what I wish someone had told me when the 2008 recession hit: three months of savings feels like a lot — right up until month two, when you realize healthcare licensing doesn’t transfer instantly and you’re waiting for a background check that takes six weeks.

The updated math:

– W2 employees with stable, in-demand skills: 6 months minimum

– W2 employees in discretionary industries (hospitality, retail, media, real estate): 9–12 months

– Side hustlers or 1099 workers with variable income: 12 months, no exceptions

Where to park it: a high-yield savings account (HYSA) or money market fund. HYSA rates have moderated as the Fed holds, but money market funds remain competitive. You want this money liquid and separate from your checking account — close enough to access, far enough that you don’t spend it.

The numbers don’t lie: if your monthly expenses are $4,500, a 6-month fund is $27,000. A 12-month fund is $54,000. Start where you are. Automate $500/month and don’t touch it.

2. Eliminate High-Interest Consumer Debt Aggressively

Recession and high-interest debt is a dangerous combination. If your income drops, minimum payments become harder to make. If rates stay elevated, your balance grows faster. You lose on both ends.

Credit card debt above 15% APR is an emergency. Treat it that way.

The method I recommend:

1. List every debt by interest rate, highest to lowest

2. Pay minimums on everything else

3. Throw every spare dollar at the highest-rate balance

4. Once it’s gone, roll that payment into the next one

This is the avalanche method, and the numbers favor it over the snowball for high-rate debt. The dopamine hit of paying off a small balance is real, but 24% APR doesn’t care about your feelings.

For guidance on how side income can accelerate this, check out our piece on side income and self-employment tax — because additional income directed at debt is one of the fastest paths out.

3. Activate or Launch a Side Hustle — Income Diversification Is a Job-Loss Buffer

A single W2 income is a single point of failure. I learned this watching colleagues get furloughed in 2020. The ones who recovered fastest weren’t the ones with the highest salaries — they were the ones who already had something else going.

A side hustle doesn’t have to be a second job. It just has to generate enough income to cover a category of expenses while you regroup. Even $500–$1,000 per month gives you breathing room.

Recession-resistant side income options:

– Freelance skills you already have (writing, spreadsheets, training, tutoring)

– Service-based work with low startup cost (cleaning, pet sitting, driving, handyman)

– Digital products (templates, courses, guides) that generate passive income once built

– AI-assisted work (research, content, automation consulting — growth area right now)

The key is to start before you need it. Building a client base or income stream takes 2–4 months of consistent effort. If you wait until you’re laid off, you’re starting from zero under pressure.

Start small and specific. Pick one skill. Find three potential clients. Quote a rate. That’s it.

4. Don’t Pause Your 401(k) — But Check Your Allocation

Here’s what I see happen every recession: people panic, stop contributing to their 401(k), and then miss the recovery entirely. I understand the impulse. When markets are falling, it feels like you’re throwing money into a hole.

But pausing contributions during a downturn is one of the most expensive financial decisions you can make. You lose:

– The employer match (that’s an instant 50–100% return on matched contributions)

– Dollar-cost averaging at lower prices (buying more shares for the same dollar amount)

– Compounding time that you can never get back

What you should do instead:

Keep contributing at least enough to capture the full employer match. Always. In every economic environment.

Then look at your allocation. If you’re 15+ years from retirement, a stock-heavy portfolio is appropriate — downturns are buying opportunities at that time horizon. If you’re within 5 years of your FIRE date, this is a good moment to review your equity/bond split and make sure you’re not taking more risk than your timeline requires.

For a full framework on how to sequence your investment contributions, see our investment order of operations guide.

5. Capture the OBBBA Tax Savings That Are Available Right Now

The One Big Beautiful Budget Act (OBBBA) included several provisions that put real money back in W2 workers’ pockets — but only if you know how to use them.

The three that matter most for W2 workers in 2026:

Overtime deduction: If you earn overtime pay, a portion of that income may now be deductible. For shift workers and hourly employees — including healthcare workers — this is meaningful. Check with your HR department or a tax professional to confirm how this applies to your situation.

SALT deduction restored: The state and local tax deduction cap was increased significantly under the OBBBA. If you live in a high-tax state and itemize deductions, this could increase your deduction substantially.

Tip income deduction: If any portion of your income comes from tips, that income may be partially or fully deductible under new OBBBA provisions.

Why this matters for recession-proofing: extra cash in your paycheck right now goes directly to your emergency fund or debt paydown — two of your highest-priority recession moves. Don’t leave this on the table.

An HSA, if you’re eligible through a high-deductible health plan, also gives you triple-tax-advantaged savings that function as a healthcare emergency fund. Learn more in our guide on the HSA triple tax advantage.

6. Build a Job-Loss Contingency Plan (Before You Need It)

Most people don’t think about what happens if they lose their job until they’ve already lost it. That’s the worst time to figure out healthcare costs, 401(k) options, and emergency contacts.

Build the plan now, when you have time to think clearly.

Your job-loss contingency plan should include:

COBRA timeline: You have 60 days from job loss to elect COBRA continuation coverage. It’s expensive — often $600–$1,500/month for a family — but it prevents a gap in coverage. Know the number before you need it. Also research marketplace plans at healthcare.gov as an alternative; depending on your income level post-job-loss, you may qualify for a subsidy.

401(k) rollover plan: When you leave an employer, you have options: leave it in the plan (if allowed), roll it to an IRA, or roll it to a new employer’s plan. Know which option fits your situation. Rolling to a traditional IRA gives you the most flexibility. Do not cash it out — you’ll owe income tax plus a 10% penalty.

Emergency contact list: Three people in your professional network who would give you an honest job lead or referral. Update your LinkedIn now, not when you’re scrambling.

Break-even budget: What’s the minimum you need to cover essential expenses? Know this number. It tells you how long your emergency fund actually lasts and which discretionary expenses get cut first.

Target timeline: How long would it realistically take to find comparable work in your field? In a recession, add 30–60% to your normal estimate.

7. Recalibrate Your FIRE Timeline for Persistent Inflation

Here’s the part that FIRE communities don’t like to talk about: if inflation stays elevated at 3–4% for several years, your FIRE number changes.

The numbers don’t lie:

The classic 4% withdrawal rule assumes your portfolio can support 25x your annual expenses indefinitely. At 2% inflation, that math holds reasonably well over a 30-year retirement. At 3.5–4% persistent inflation, you either need a larger portfolio or a more flexible withdrawal strategy.

What this means practically:

If you calculated your FIRE number at 2% inflation, run it again at 3.5%. For most people, this increases the target by 15–25%. That might mean 1–3 more years of accumulation, or a more aggressive savings rate for the next few years.

Options to close the gap:

– Increase your savings rate by 2–5% while income is stable

– Add a side income stream that continues into early retirement (the “FIRE with income” model)

– Use a flexible withdrawal rate (3.5% instead of 4%) in the early years of retirement

– Build a larger cash/short-term bond buffer (2–3 years of expenses) to avoid selling equities during a downturn

For a full walkthrough of how to calculate and pressure-test your FIRE number, see our guide: FIRE Number: How Much Do You Actually Need?

The goal isn’t to be pessimistic — it’s to be accurate. A plan that accounts for real-world inflation is a plan you can actually execute.

Frequently Asked Questions

Q: Should I stop investing in my Roth IRA if a recession hits?

No. Keep contributing. A recession means asset prices are lower, which means your Roth contributions buy more. Your future self will thank you. Pause discretionary spending, not tax-advantaged investing.

Q: How quickly should I build up my emergency fund vs. paying off debt?

Build a $1,000–$2,000 starter emergency fund first. Then attack high-interest debt (anything above 8–10% APR). Once high-interest debt is cleared, build your full 6–12 month emergency fund. If you have an employer 401(k) match, always contribute enough to capture it while doing all of the above.

Q: Is a HYSA really safe if a bank fails?

Yes. FDIC insurance covers up to $250,000 per depositor per institution. Keep your emergency fund at an FDIC-insured bank and you’re protected. Money market funds at major brokerages are also generally very safe, though they are not FDIC-insured — they’re covered by SIPC.

Q: What if I can’t afford to save 6 months of expenses right now?

Start with $500. Then $1,000. Direction matters more than speed. Automate a small transfer to a separate HYSA the day after each paycheck. Even $100/month becomes $1,200 in a year without thinking about it. The goal is to build the habit and the buffer simultaneously.

Q: Should I be moving my investments to cash given recession risk?

Not unless you’re within 1–2 years of needing the money. Timing the market is statistically harder than just staying invested. The data consistently shows that missing the 10 best market days in a given decade — which often happen right after the worst days — costs you more than the downturn itself. Stay the course. Adjust allocations based on your timeline, not fear.

Bottom Line

The best recession-proofing strategy is the one you build before the recession arrives. FIRE practitioners have always understood this: financial independence isn’t just about retiring early — it’s about never being financially desperate regardless of what the economy does.

Pick the two moves on this list that you haven’t done yet and start there. Not everything at once. Two things, this week.

If you want a framework for how all of these pieces fit together, subscribe to the Aedilis newsletter — we break down personal finance for W2 workers and side hustlers once a week, in plain English.

The information on this page is for educational purposes only and does not constitute personalized financial, tax, or investment advice. Always consult a qualified professional before making financial decisions. Tax laws change frequently. This article reflects rules as of June 2026. Verify current rules at IRS.gov or consult a tax professional.